TL;DR:

- Preparation of thorough environmental, financial, and legal documents is essential for GTA sale-leasebacks.

- Structuring the deal for IFRS 16 compliance and market competitiveness is complex but critical.

- Local market knowledge significantly impacts deal outcomes and long-term operational flexibility.

Imagine you own a 50,000-square-foot warehouse in Brampton. The building is paid off, the operation is running well, but growth capital is locked inside those walls. A sale-leaseback lets you sell the property to an investor, pocket the proceeds, and sign a long-term lease to stay put and keep operating. It sounds straightforward. In practice, GTA industrial owners routinely lose deals to environmental surprises, IFRS 16 structuring errors, and lease terms that strangle flexibility years later. This guide walks you through every critical step so you can move forward with confidence.

Table of Contents

- What you need before starting a sale-leaseback

- Key steps in the GTA industrial sale-leaseback process

- Regulatory, tax, and accounting essentials

- Common pitfalls and GTA-specific nuances

- What to expect after closing: lease management and future options

- A hard-earned truth: the optimal sale-leaseback is local and adaptive

- Ready to optimise your GTA industrial asset?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Preparation is crucial | Gather all documents, confirm environmental compliance, and know your minimum goals before starting. |

| Follow a clear process | Move step by step through market analysis, deal structuring, due diligence, negotiation, and closing. |

| Understand IFRS criteria | IFRS 16 rules are strict; leasing terms and sale structure must qualify as a true sale or the deal can fail. |

| Avoid common mistakes | Most deals collapse over lease structuring, missed reports, or ignoring local market realities. |

| Plan post-closing strategy | Ongoing lease management and flexibility are essential to maximise sale-leaseback benefits. |

What you need before starting a sale-leaseback

The quality of your preparation determines the quality of your outcome. Buyers of GTA industrial assets are sophisticated. They will probe every document, every environmental record, and every financial statement before committing capital. Showing up underprepared signals risk, and risk kills pricing.

Start by assembling your core document package:

- Title and ownership documents: A clean title search, any registered encumbrances, and confirmation of ownership structure

- Operating statements: At least three years of audited or reviewed financials demonstrating stable revenue and occupancy costs

- Existing lease agreements: If tenants occupy any portion of the building, buyers need full lease abstracts

- Property condition reports: Recent roof, HVAC, and structural assessments showing deferred maintenance levels

- Environmental assessments: A current Phase I Environmental Site Assessment (ESA) is the baseline; many GTA industrial sites also require a Phase II ESA given historic land use

Environmental due diligence is especially critical in GTA industrial transactions because the region carries decades of manufacturing and logistics history. Contamination liability can transfer to a buyer, so most institutional purchasers will not proceed without a clean or remediated environmental file. Budget for this early.

Beyond documents, you need to demonstrate tenant covenant strength. In a sale-leaseback, you become the tenant. Buyers are essentially underwriting your business as much as the building. Prepare a business credit profile, recent financial statements, and a clear narrative about your operational stability and growth trajectory.

| Prerequisite | Why it matters | Typical timeline to prepare |

|---|---|---|

| Phase I/II ESA | Liability transfer protection for buyer | 4-8 weeks |

| Audited financials (3 years) | Proves tenant covenant strength | 2-4 weeks to compile |

| Title search and survey | Confirms clean ownership | 1-2 weeks |

| Property condition report | Sets repair/pricing expectations | 2-3 weeks |

| IFRS 16 eligibility review | Confirms deal qualifies as a true sale | 1-2 weeks with advisors |

Understanding GTA ESG requirements is also increasingly relevant. Institutional buyers are screening acquisitions against sustainability benchmarks, and a building with poor energy ratings or deferred green upgrades may attract a pricing discount.

Pro Tip: Know your minimum capital goal before you begin. If you need $8 million to fund expansion, work backwards from that number to understand what sale price and lease rate structure you can accept. Entering negotiations without this anchor leads to deals that feel like wins but leave you cash-constrained.

Working with an industrial real estate expert from the outset dramatically reduces preparation time and helps you avoid assembling documents that buyers will ultimately reject.

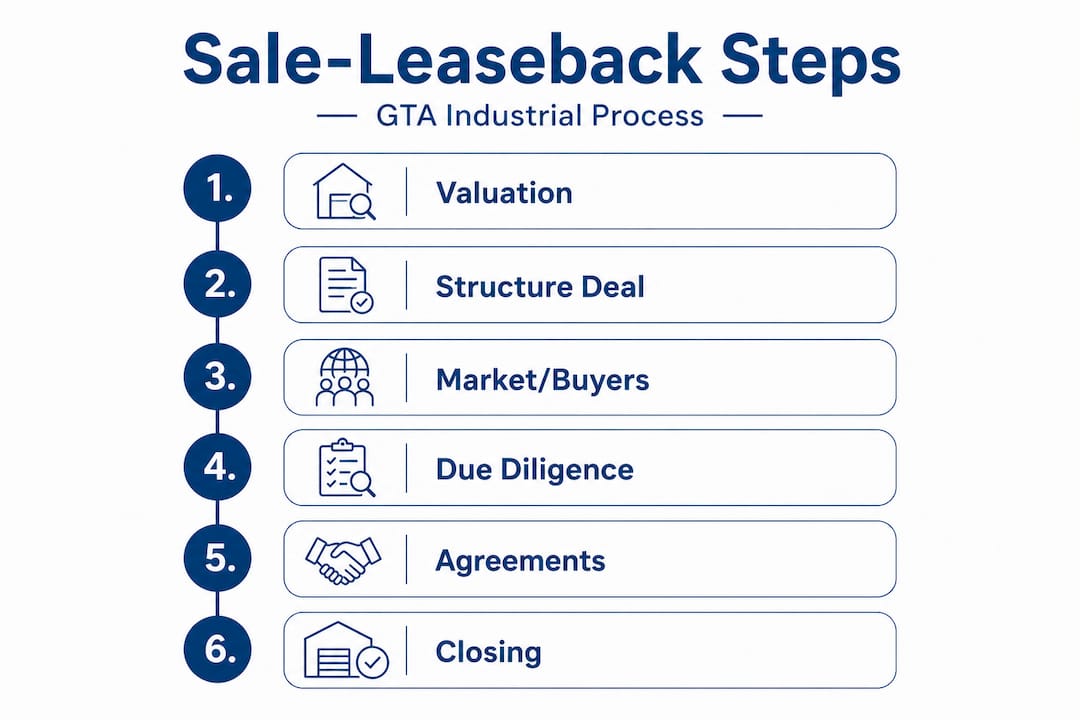

Key steps in the GTA industrial sale-leaseback process

Now that your prerequisites are in order, here is an actionable sequence for the GTA sale-leaseback process.

Step 1: Property and market assessment Commission an independent valuation of your property based on current GTA industrial market conditions. Cap rates, vacancy rates, and comparable sales in your specific submarket (Mississauga Airport Corridor, Vaughan, Durham Region) will drive your sale price expectation. Do not rely on assessed value or what a neighbour sold for three years ago.

Step 2: Structure the deal This is where most owners underestimate complexity. You need to determine the sale price, the initial lease rate, the lease term length, rent escalation provisions, and renewal options. Critically, the transaction must qualify as a true sale under IFRS 16. That means no repurchase options covering the full asset life, and all terms must reflect market conditions. A deal structured with below-market rent or a guaranteed buyback right may be reclassified as financing rather than a sale, which eliminates the accounting and capital benefits entirely.

Step 3: Go to market or target buyers Your advisor will either run a targeted off-market process with institutional buyers, private investors, or REITs, or list the property publicly. In the GTA, institutional buyers typically seek net leases of 10 to 15 years with investment-grade tenants. Private buyers may accept shorter terms or more operational flexibility. Matching buyer profile to your lease structure needs is a strategic decision, not just a pricing exercise.

Step 4: Buyer due diligence Buyer due diligence in GTA industrial transactions is heavily focused on three areas: tenant credit quality, environmental and condition reports, and lease structure compliance. Expect 30 to 60 days of scrutiny. Buyers will order their own Phase I/II assessments, review your financials independently, and verify that the proposed lease terms satisfy IFRS 16 requirements. Any gap in your preparation package surfaces here.

Step 5: Negotiate and finalise agreements The purchase and sale agreement and the lease agreement are negotiated simultaneously. Key lease terms to protect include: rent escalation caps, capital expenditure responsibilities, sublease and assignment rights, and early termination provisions. Do not treat the lease as an afterthought to the sale. You will live under those terms for a decade or more.

Step 6: Closing and capital release Once conditions are waived and both agreements are executed, closing follows standard Ontario commercial real estate timelines. Capital is released upon title transfer. Your lease commences simultaneously, and you transition from owner to tenant on day one.

| Deal stage | Owner's priority | Buyer's priority |

|---|---|---|

| Valuation | Maximise sale price | Confirm cap rate and yield |

| Lease structuring | Flexibility and renewal options | Long term, fixed escalations |

| Due diligence | Fast, clean disclosure | Thorough credit and environmental review |

| Negotiation | Protect operational rights | Minimise landlord obligations |

Unlocking capital with sale-leasebacks requires treating both the sale and the lease as equally important negotiations. Owners who focus exclusively on the sale price often regret the lease terms they accepted.

Pro Tip: Request a lease commencement date that gives you time to complete any tenant improvements or operational transitions before rent obligations begin. Even 30 to 60 days of rent-free period at commencement can meaningfully reduce your transition costs.

Regulatory, tax, and accounting essentials

With step-by-step logistics outlined, attention must turn to compliance and documentation detail, where deals most often fail.

IFRS 16 is the accounting standard that governs how sale-leasebacks appear on financial statements for companies reporting under International Financial Reporting Standards. Post-2019, IFRS on-balance sheet changes require most leases to be recognised as right-of-use assets and corresponding liabilities. This increases structuring complexity because the accounting treatment of your leaseback directly affects your profit and loss profile and balance sheet ratios.

Key IFRS 16 rules to understand:

- True sale requirement: The transaction must transfer control of the asset. Repurchase options that cover the full economic life of the property disqualify it as a sale.

- Market terms test: If the sale price or lease rate deviates significantly from market, the gain or loss on sale is adjusted. Inflated sale prices paired with above-market rent are flagged and adjusted by auditors.

- Variable lease payments: 2024 amendments clarified how variable lease payments are measured at commencement and reassessed. If your lease includes CPI-linked escalations or variable components, these must be structured carefully to avoid unintended accounting consequences.

"A sale-leaseback that fails the IFRS 16 true sale test is reclassified as a financing arrangement. The seller retains the asset on its balance sheet and recognises a financial liability instead of sale proceeds. The capital release benefit disappears entirely."

On the tax side, GTA industrial owners face three primary considerations. First, HST applies to the sale of commercial real property in Ontario. Structuring the transaction as a going concern may allow HST to be avoided, but this requires careful legal advice. Second, capital gains will arise if the sale price exceeds your adjusted cost base. The inclusion rate and your corporate tax position will determine the net proceeds after tax. Third, property tax adjustments are reconciled at closing, and your ongoing lease will specify how realty taxes are treated, typically passed through to you as tenant under a net lease structure.

Staying current on GTA industrial trends matters here because municipal assessment cycles and tax rate changes in specific GTA nodes can meaningfully affect your occupancy cost projections over a 10 to 15-year lease.

Pro Tip: Engage a tax advisor with commercial real estate transaction experience before signing any term sheet. The difference between a well-structured and a poorly structured sale from a tax perspective can represent hundreds of thousands of dollars in avoidable liability.

Common pitfalls and GTA-specific nuances

Once legal and compliance boxes are checked, it is just as critical to know how deals can and often do go wrong.

Failing the IFRS 16 audit: Owners sometimes negotiate lease terms that feel commercially reasonable but inadvertently include provisions that reclassify the deal as financing. A repurchase option at a fixed price, a lease term covering nearly all of the building's remaining useful life, or a guaranteed residual value can each trigger reclassification. Have your auditors review the proposed lease structure before you sign.

Undetected environmental liabilities: GTA industrial land carries real contamination risk. A Phase I ESA that reveals a recommendation for Phase II investigation is not a deal-killer, but it is a negotiating event. Buyers will price environmental risk aggressively. Addressing known issues before going to market almost always produces better pricing than leaving them for buyers to discover.

Overvaluing the property: Market softening in the GTA, with rising vacancy in some submarkets, may favour sellers in terms of buyer appetite, but cap rates have remained relatively stable. Owners who anchor to peak 2021 or 2022 valuations will find buyers unwilling to meet expectations. An independent appraisal based on current data is essential.

Inflexible lease terms: Signing a 15-year lease with no sublease rights, no assignment clause, and no early termination option locks you into an obligation that could become a serious liability if your business contracts, relocates, or is acquired. Negotiate these protections upfront, even if they cost you slightly on the sale price.

- Require sublease and assignment rights with landlord consent not to be unreasonably withheld

- Include a capital expenditure responsibility schedule so you know exactly what you are responsible for maintaining

- Negotiate market rent review mechanisms rather than fixed escalations if your business cycle is cyclical

Market intelligence for GTA investors and industrial property trends should inform your lease rate expectations before you enter any negotiation.

Pro Tip: Never commit to a lease term longer than your business planning horizon. If your five-year plan includes a possible acquisition, relocation, or significant footprint change, a 15-year leaseback without exit provisions is a strategic trap.

What to expect after closing: lease management and future options

With an eye to the future, here is what to plan for once the ink dries on your sale-leaseback agreement.

Your relationship with the property shifts fundamentally on closing day. You are now a tenant with contractual obligations rather than an owner with discretionary control. Annual lease management responsibilities include:

- Paying base rent and operating cost pass-throughs on time and in full

- Maintaining the property in the condition specified by the lease

- Carrying the insurance coverages required under the lease terms

- Providing annual financial statements to the landlord if your covenant is subject to ongoing review

- Tracking and reporting any environmental incidents or changes in use

IFRS compliance does not end at closing. Your right-of-use asset and lease liability must be remeasured whenever there is a lease modification, a change in lease term, or a reassessment of variable payments. Annual audits will scrutinise these calculations. Build internal processes to track lease data accurately from day one.

Flexibility versus long-term lease commitment risk is the central tension of every sale-leaseback. The capital you unlock is real and immediate. The lease obligation is also real and long-term. Managing that tension well means actively monitoring your space utilisation and renegotiating terms when market conditions shift in your favour.

Subleasing is one of the most powerful tools available to you as a tenant. If your footprint needs shrink, key concepts for subleasing can help you offset lease costs by bringing in a subtenant for unused space. This requires landlord consent in most leases, which is why negotiating a reasonable consent standard at the outset is so important.

Looking further ahead, a well-structured sale-leaseback positions you for future asset reallocation. The capital released can fund acquisitions in other markets, technology investments, or debt reduction. Your industrial footprint remains stable operationally while your balance sheet gains flexibility.

Pro Tip: Schedule a lease review with your real estate advisor every two to three years. GTA market conditions change, and a lease that was at-market in 2026 may be above-market by 2029. Early renegotiation conversations, even informal ones, keep you positioned to act when leverage shifts.

A hard-earned truth: the optimal sale-leaseback is local and adaptive

Here is something national advisory firms rarely tell you. Generic sale-leaseback templates built for Calgary or Vancouver industrial assets do not translate cleanly to the GTA. The regulatory environment, the buyer pool, the environmental risk profile, and the submarket dynamics in Mississauga are materially different from those in Markham or Hamilton. Applying a cookie-cutter approach to a GTA transaction is how owners leave money on the table or walk into lease terms that do not fit their business reality.

Local expertise changes the outcome in specific, measurable ways. An advisor who knows that a particular Vaughan submarket has three competing listings will price your asset differently than one working from a national cap rate average. An advisor who understands the environmental history of a specific industrial corridor will anticipate Phase II requirements before buyers raise them, giving you time to manage the narrative rather than react to it.

Lease term flexibility is another area where local knowledge matters enormously. Institutional buyers in the GTA have specific preferences about lease structure that differ from private buyers. Knowing which buyer type to target for your specific asset and your specific operational needs is a strategic decision that requires GTA real estate expertise, not just a general understanding of sale-leaseback mechanics.

The owners who achieve the best outcomes treat the sale-leaseback as a business strategy, not a real estate transaction. They start with their operational and financial goals, work backwards to the deal structure that achieves those goals, and choose advisors who understand both the local market and the regulatory framework deeply enough to protect them at every stage.

Ready to optimise your GTA industrial asset?

Turning a sale-leaseback from concept to closed transaction requires precise preparation, local market knowledge, and experienced negotiation on both the sale and the lease. The difference between a deal that truly unlocks your capital and one that creates long-term operational constraints often comes down to the quality of advice you receive before you sign anything.

Michael Law Real Estate specialises in GTA industrial sale-leasebacks, investment sales, and tenant representation across every major industrial corridor in the region. Whether you are exploring GTA industrial listings in Markham, evaluating Milton industrial opportunities, or ready to see available properties across the GTA, our team brings the local intelligence and transaction experience to help you capture maximum value. Contact us for a confidential consultation and let us build the right structure for your asset and your business.

Frequently asked questions

What disqualifies a sale-leaseback under IFRS 16?

Any repurchase option covering the entire asset life or non-market lease terms can disqualify a sale-leaseback under IFRS 16, reclassifying it as a financing arrangement rather than a true sale.

How long does a typical sale-leaseback process take in the GTA?

Most GTA industrial sale-leasebacks are completed in 60 to 120 days, assuming environmental reports, financial statements, and due diligence materials are prepared and ready before going to market.

Will a sale-leaseback affect my financial statements?

Yes. Post-2019 IFRS changes require most leases to be recognised on-balance sheet as right-of-use assets and lease liabilities, which affects your debt ratios, depreciation charges, and profit profile.

Why is environmental due diligence so important in GTA industrial deals?

Buyers require recent Phase I/II assessments because GTA industrial land carries significant historic contamination risk, and environmental liability can transfer with the property if not properly disclosed and resolved before closing.