Many GTA industrial property owners assume that selling their building means handing over the keys and walking away. That assumption costs them millions in untapped capital. A sale-leaseback is a transaction where an owner sells an industrial property to an investor and immediately leases it back under a long-term agreement, unlocking capital while retaining full operational use. Far from losing control, you keep running your facility exactly as before. This guide breaks down how these deals work in the GTA, what the numbers actually look like, and how to avoid the pitfalls that catch even experienced owners off guard.

Table of Contents

- What is a sale-leaseback in industrial real estate?

- How GTA industrial sale-leasebacks actually work

- Key benefits and risks: GTA market context

- Case studies: Recent GTA industrial sale-leasebacks

- Smart strategies for GTA industrial owners and tenants

- Our take: Why sale-leaseback in Toronto is still evolving

- Explore expert guidance for GTA industrial sale-leaseback

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Capital unlock with control | Sale-leaseback lets GTA industrial owners access liquidity while keeping operational use of their assets. |

| Compliance matters | IFRS 15/ASC 606 rules determine if a sale-leaseback qualifies, impacting gains and accounting treatment. |

| Risks vary by asset | Lease rates, audit complexity, and market maturity shape the outcome—mission-critical assets fare best. |

| Local market opportunities | GTA's high valuations and evolving sale-leaseback trends benefit strategic owners and tenants. |

| Expert advice essential | Professional guidance optimises terms and avoids common pitfalls in sale-leaseback agreements. |

What is a sale-leaseback in industrial real estate?

A sale-leaseback involves two parties: a property owner who needs liquidity and an investor seeking stable, long-term income. The owner sells the property to the investor, then signs a lease to continue occupying and operating from the same facility. Nothing changes on the floor of your warehouse or manufacturing plant. What changes is your balance sheet.

This is fundamentally different from a standard lease or an outright sale. In a traditional sale, you vacate. In a standard lease, you never owned the asset. A sale-leaseback sits in between: you monetise the real estate without disrupting operations. For GTA industrial owners sitting on properties that have appreciated sharply since 2020, this distinction matters enormously.

The typical structure looks like this:

- Owner sells the industrial property at current market value

- Investor acquires the asset and becomes the landlord

- Owner-turned-tenant signs a long-term net lease, often 10 to 20 years

- Capital proceeds are redeployed into core business operations, debt reduction, or growth

- Lease terms are negotiated upfront, including renewal options and rent escalation clauses

Keeping an eye on industrial property trends is essential before entering any sale-leaseback, because market timing directly affects the sale price and the lease rate you lock in for the long term.

"A sale-leaseback is not a retreat from your property. It is a deliberate decision to separate the value of real estate from the value of your business operations."

For GTA industrial owners, this tool is particularly relevant. Land values in Brampton, Mississauga, and Vaughan have surged, and many owner-operators are sitting on real estate worth far more than their business generates annually. Sale-leaseback converts that dormant equity into working capital.

How GTA industrial sale-leasebacks actually work

The mechanics behind a sale-leaseback are more technical than most owners expect. Getting them wrong creates audit exposure and can unwind the tax and accounting benefits entirely.

The first step is confirming the transaction qualifies as a genuine sale under IFRS 15 or ASC 606. This means control of the asset must transfer fully to the buyer. If the seller retains a repurchase option or the buyer cannot direct the use of the property, the deal fails the control transfer test and cannot be recorded as a sale. This is a critical distinction that affects how gains are recognised on your financial statements.

Once the sale qualifies, the leaseback is classified as either an operating lease or a finance lease. The classification depends on the lease term and a present value test. If the present value of lease payments exceeds 90% of the property's fair value, the leaseback is treated as a finance lease, which limits gain recognition. Partial gain recognition applies only to the rights actually transferred to the buyer.

Here is a simplified overview of the key decision points:

- Assess control transfer under IFRS 15/ASC 606

- Confirm no repurchase options exist that would disqualify the sale

- Run the present value test on future lease payments versus fair value

- Classify the leaseback as operating or finance

- Recognise gain only on the portion of rights transferred

| Step | Key question | Risk if skipped |

|---|---|---|

| Control transfer | Does the buyer fully control the asset? | Deal reclassified as financing |

| PV test | Do payments exceed 90% of fair value? | Finance lease treatment applies |

| Gain recognition | What rights were transferred? | Overstated gains, audit exposure |

For GTA industrial investment sales, understanding these steps is non-negotiable. Owners who skip the accounting analysis often face restatements later. A solid net lease guide also helps clarify how lease structures interact with these accounting rules.

Pro Tip: Engage your auditors before signing any sale-leaseback term sheet. Retroactive accounting adjustments are expensive and avoidable.

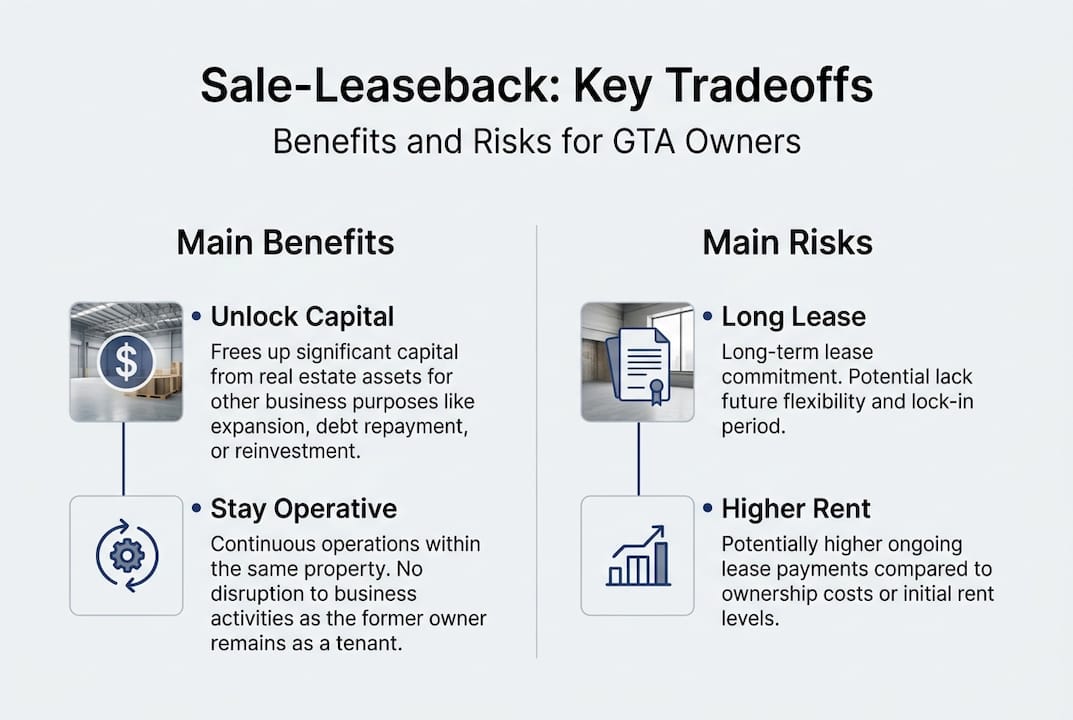

Key benefits and risks: GTA market context

Sale-leasebacks are growing in popularity across the GTA, and for good reason. But they carry real risks that owners must weigh carefully before proceeding.

The core benefits:

- Immediate liquidity without disrupting operations

- Off-balance sheet financing under operating lease classification, improving financial ratios

- Capital redeployment into higher-return business activities

- Continued facility use under agreed lease terms, preserving operational continuity

- Potential tax advantages depending on the gain recognition structure

The GTA market is less mature than US counterparts, which creates genuine deal-making opportunities for owners and investors who understand the landscape. High valuations following the post-2020 industrial boom, combined with rising interest rates, have made sale-leaseback an attractive alternative to traditional debt financing.

Current market data reinforces this. GTA industrial cap rates for sale-leasebacks sit around 6 to 7%, with sale prices ranging from $339 to $357 per square foot in Q2 to Q3 2025. Vacancy rates have stabilised near 4.4 to 4.5%, supporting stable yields for investors.

| Factor | Benefit | Risk |

|---|---|---|

| Liquidity | Immediate capital access | Long-term lease obligation |

| Lease rate | Locked in at negotiation | May exceed cap rate over time |

| Accounting | Off-balance sheet (operating) | Finance lease reclassification |

| Operations | No disruption | Renewal risk at lease expiry |

The real risks are often underestimated. If the lease rate you agree to today exceeds the cap rate implied by the sale price, you are effectively overpaying for occupancy over the lease term. Audit complexity is another concern, particularly for GTA owners unfamiliar with IFRS 15 requirements.

For industrial tenants in mission-critical facilities, the calculus is different. When your location is irreplaceable and your operations depend on that specific site, the lease obligation becomes a manageable cost of retaining access to a strategic asset.

Pro Tip: Run a detailed net present value comparison between the sale-leaseback lease cost and the cost of alternative financing before committing. The numbers often surprise owners.

Case studies: Recent GTA industrial sale-leasebacks

Theory becomes real when you look at what major players have actually done in the GTA market. Two transactions stand out as instructive examples.

Canadian Tire and Prologis, Brampton (2024)

In 2024, Canadian Tire sold its Brampton distribution facility, a 1.5 million square foot asset, to Prologis for $258 million. The deal is one of the largest single-asset industrial transactions in Canadian history. Canadian Tire retained operational use through a leaseback arrangement, preserving its distribution network while unlocking substantial capital.

| Transaction detail | Canadian Tire / Prologis | Polytainers / W.P. Carey |

|---|---|---|

| Location | Brampton, GTA | GTA portfolio |

| Size | 1.5M sq ft | 496,000 sq ft |

| Sale price | $258M | $93M |

| Lease term | Long-term leaseback | 20-year leases |

Polytainers and W.P. Carey

W.P. Carey acquired the Polytainers GTA industrial portfolio for $93 million, covering 496,000 square feet across multiple properties. The 20-year lease terms locked in stable income for the investor while giving Polytainers a long runway of operational certainty.

Key takeaways from both deals:

- Scale matters but is not a prerequisite. Both large and mid-size portfolios qualify.

- Long lease terms (15 to 20 years) are standard and give investors the income stability they require.

- Pricing reflects market strength. Both deals priced at or above prevailing GTA benchmarks.

- Operational continuity was preserved in both cases, validating the core premise of sale-leaseback.

These transactions are shaping GTA industrial real estate trends and setting pricing benchmarks that smaller owners can reference when evaluating their own assets.

Smart strategies for GTA industrial owners and tenants

Knowing the mechanics and the market is only half the battle. Executing a sale-leaseback well requires disciplined preparation and sharp negotiation.

Evaluate suitability first:

- Assess your capital need. Is the liquidity you would unlock worth a long-term lease obligation?

- Confirm operational dependency. Is this facility mission-critical, or could you relocate if lease costs rise?

- Get an independent valuation. Never enter negotiations without knowing your property's current market value.

- Model the lease cost. Calculate the total lease payments over the full term and compare to alternative financing costs.

- Review your accounting framework. Confirm whether IFRS or ASPE applies to your financial statements before structuring the deal.

Negotiation tactics that matter:

- Push for renewal options at predetermined rates to protect against market rent spikes at lease expiry

- Negotiate rent escalation caps tied to CPI rather than open-market resets

- Align the cap rate with current GTA benchmarks (6 to 7%) to avoid overpaying through the lease

- Include subletting rights in case your operational footprint changes

Common mistakes to avoid:

- Accepting a lease rate without modelling the long-term cost relative to the sale proceeds

- Overlooking renewal terms until it is too late to renegotiate

- Failing to engage legal counsel experienced in GTA advisory services for commercial real estate

Sale-leaseback is best suited to mission-critical assets where operational continuity outweighs the cost of the lease obligation. Engaging an industrial real estate expert early in the process reduces the risk of costly errors in valuation and lease structuring.

Pro Tip: Request comparable lease transactions from your advisor before finalising any lease rate. Market data is your strongest negotiating tool.

Our take: Why sale-leaseback in Toronto is still evolving

Here is what most articles on this topic miss: the GTA sale-leaseback market is genuinely less mature than its US counterpart, and that cuts both ways. Owners face fewer established benchmarks, which makes pricing negotiations harder. But investors face the same gap, which means motivated sellers with strong assets can command better terms than they might in Chicago or Los Angeles.

The post-2020 valuation surge has made sale-leaseback attractive for GTA owners who want liquidity without debt. Rising rates have reinforced that appeal. But we have seen owners rush into these deals without fully modelling the lease cost, only to find that the long-term obligation erodes the capital benefit they expected.

The deals that work best share one trait: the property is genuinely irreplaceable for the operator. When your Brampton distribution hub or Mississauga manufacturing plant cannot be easily substituted, the lease obligation is a price worth paying. When the asset is fungible, the calculus shifts.

For a deeper look at how GTA investment sales are evolving, the data tells a clear story: institutional capital is moving into GTA industrial, and sale-leaseback is one of the primary vehicles. Owners who understand this dynamic are better positioned to negotiate from strength.

Explore expert guidance for GTA industrial sale-leaseback

Sale-leaseback decisions carry long-term financial and operational consequences. Getting the structure, pricing, and lease terms right from the start is what separates a successful transaction from a costly one.

At Michael Law Real Estate, we work with GTA industrial owners and tenants to navigate exactly these decisions, from initial asset valuation through lease negotiation and closing. Whether you are evaluating your first sale-leaseback or refining terms on an existing deal, our advisory team brings transaction experience and local market data to every engagement. Explore our GTA property listings or connect with us directly to discuss how a sale-leaseback strategy could work for your specific asset and operational needs.

Frequently asked questions

What types of industrial properties qualify for sale-leaseback in the GTA?

Mission-critical industrial properties such as distribution centres, manufacturing plants, and logistics hubs are best suited, particularly when the owner retains operational use under a long-term lease and the asset has strong income potential for investors.

How are sale-leaseback gains treated under accounting rules?

Only the portion of gain relating to rights transferred to the buyer is recognised, with IFRS 15/ASC 606 requiring full control transfer and no repurchase options for the transaction to qualify as a sale.

What are typical cap rates and pricing ranges for GTA industrial sale-leasebacks?

Recent GTA transactions show cap rates of 6 to 7% and sale prices ranging from $339 to $357 per square foot, with industrial vacancy stabilised near 4.4 to 4.5% as of mid-2025.

Who benefits most from industrial sale-leaseback in Toronto?

Owners who need liquidity but cannot afford operational disruption benefit most, particularly when the leased facility is mission-critical and alternative locations are scarce or impractical.

What are common mistakes in sale-leaseback agreements?

The most frequent errors involve miscalculating lease costs relative to the sale proceeds and failing to negotiate renewal options, both of which erode the financial benefit over the lease term.