TL;DR:

- A sale-leaseback allows property owners to unlock capital while maintaining operational control through leasing. Proper analysis of accounting treatment, physical condition, and market fundamentals is crucial to avoid costly mistakes. Comprehensive due diligence and strategic financial evaluation ensure the deal's long-term value in the competitive GTA industrial market.

Picture this: you own a 50,000-square-foot warehouse in Brampton. The building is worth $12 million, but that capital is sitting idle while your operating costs climb and your lender is tightening credit terms. A buyer approaches with a sale-leaseback offer. You sell, pocket the proceeds, and lease back the space you need. Sounds straightforward. But without understanding how to properly analyse the accounting treatment, economic fundamentals, and due diligence requirements, you could walk into a deal that costs far more than it unlocks. This guide walks you through every critical step.

Table of Contents

- What is a sale-leaseback deal and why consider one?

- Preparing for analysis: Data, documents, and prerequisites

- Step-by-step: Accounting analysis and classification

- Economic deal analysis: What numbers really matter?

- Due diligence and risk management essentials

- Why economic and accounting analysis both matter more than most think

- Next steps: How expert guidance helps you win on GTA leaseback deals

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| IFRS classification is critical | Sale-leasebacks must meet strict rules to be recognized as a sale; otherwise they're treated as financing. |

| Prepare all due diligence | Gather legal, environmental, and zoning documents up front to avoid costly surprises in GTA deals. |

| Economic analysis guides value | Assess cap rates, market rent, and risk allocation to make profitable leaseback decisions. |

| Risk management is a must | Always stress-test exit and contingency scenarios before committing to any leaseback. |

What is a sale-leaseback deal and why consider one?

A sale-leaseback is a transaction where a property owner sells an asset to a buyer and simultaneously enters a lease to continue occupying it. The seller becomes the tenant; the buyer becomes the landlord. The original owner keeps operational continuity while converting a fixed asset into liquid capital.

In the GTA industrial market, these deals have grown considerably popular. Tight vacancy rates, strong investor appetite, and rising land values have made industrial properties attractive to institutional buyers. For owner-operators in logistics, manufacturing, or warehousing, a leaseback can free up capital for equipment, expansion, or debt reduction without forcing a relocation.

A critical distinction: sale-and-leaseback accounting applies only if the transfer qualifies as a true sale. If it does not, the entire arrangement is treated as a financing transaction, not a sale. This matters enormously for your balance sheet, tax position, and how you report the transaction to stakeholders.

When does a sale-leaseback make sense for GTA industrial owners?

- You need capital for growth but want to avoid traditional debt financing

- Your balance sheet would benefit from converting a fixed asset to cash

- You want to lock in a long-term lease at today's market rents before further escalation

- You are planning an exit from ownership but need operational continuity

- You want to redeploy capital into higher-yielding investments or acquisitions

Understanding the industrial sale-leaseback strategy in the GTA context is the first step. But knowing when to use it is just as important as knowing how.

| Feature | Sale-leaseback | Traditional financing | Pure asset sale |

|---|---|---|---|

| Capital unlocked | Full property value | Partial (LTV limited) | Full property value |

| Operational continuity | Yes | Yes | No |

| Balance sheet impact | Asset removed | Liability added | Asset removed |

| Ongoing occupancy cost | Lease payments | Mortgage payments | None (must relocate) |

| Flexibility | Moderate | Low | High |

The net lease guide explains how lease structures affect ongoing cost responsibilities, which is directly relevant when negotiating leaseback terms.

Preparing for analysis: Data, documents, and prerequisites

Before you can assess whether a leaseback makes financial sense, you need the right information in front of you. Incomplete data leads to flawed analysis. In the GTA, where deals move quickly and competition is fierce, walking into negotiations without a full document set is a serious disadvantage.

Industrial real estate due diligence always starts with the physical and legal foundation of the property. Even if the lease will shift many operating costs to the tenant, the buyer and landlord must still assess physical condition, legal encumbrances, zoning compliance, and environmental status as core diligence items.

Key documents to gather before analysis:

- Registered title and any encumbrances or easements

- Current zoning certificate and permitted uses

- Phase I Environmental Site Assessment (ESA), and Phase II if flagged

- Property condition assessment or building inspection report

- Survey showing boundaries, encroachments, and easements

- Existing leases, licences, or occupancy agreements

- Municipal property tax records and outstanding work orders

- Capital expenditure history and deferred maintenance schedule

| Document | Purpose | Typical source |

|---|---|---|

| Title search | Confirms ownership and encumbrances | Land Registry Office |

| Zoning certificate | Confirms permitted industrial use | Local municipality |

| Phase I ESA | Identifies environmental risk | Qualified environmental consultant |

| Property condition report | Identifies structural or mechanical issues | Building inspector |

| Survey | Confirms boundaries and encroachments | Licensed Ontario land surveyor |

Pro Tip: Start your environmental assessment early. In the GTA, qualified ESA consultants are in high demand, and delays of four to six weeks are common. A stalled environmental review can derail deal timelines and give the other party leverage to renegotiate terms.

The property acquisition checklist provides a broader framework for what to gather before committing to any industrial transaction, including leasebacks.

Step-by-step: Accounting analysis and classification

With your documents assembled, the next task is determining how the transaction will be classified under accounting standards. This is not just a technical formality. The classification determines whether you recognise a gain on sale, how the leaseback is recorded on your books, and what your ongoing financial statements look like.

Under IFRS 16, the governing standard for most Canadian public companies and many private entities that follow IFRS, a sale-leaseback is classified as either a true sale or a financing arrangement. The test hinges on whether control of the asset transfers to the buyer using the IFRS 15 criteria for revenue recognition. If control does not transfer, the entire deal is treated as a financing arrangement under IFRS 9, with no gain recognised and the proceeds recorded as a financial liability.

Steps to classify your leaseback transaction:

- Confirm the applicable standard. Determine whether your entity reports under IFRS, ASPE (Accounting Standards for Private Enterprises), or another framework. IFRS 16 applies to IFRS reporters; ASPE has different rules.

- Apply the IFRS 15 control test. Ask whether the buyer obtains control of the asset. Consider: does the buyer have the right to direct the use of the property and obtain substantially all of its economic benefits?

- Review the leaseback terms for indicators of retained control. If the seller-lessee retains the right to repurchase, or if the lease is structured as a full payout lease, control may not transfer.

- Assess whether sale price and rent are at market. Off-market terms require adjustments. If the sale price is above market, the excess is treated as additional financing from the buyer. If rent is above market, the excess is treated as a prepayment of rent.

- Calculate the right-of-use (ROU) asset and lease liability. If the deal qualifies as a sale, the seller-lessee recognises an ROU asset representing only the retained portion of the asset.

- Determine gain or loss recognition. Gain or loss is limited to the rights transferred to the buyer. Any gain relating to the retained ROU asset is eliminated.

Review subleasing concepts if your leaseback involves a head lease with a sublease component, as layered structures add complexity to the classification analysis.

Pro Tip: If your proposed rent deviates more than 10 to 15 percent from current GTA market rates, get a professional accounting review before signing. Off-market terms trigger measurement adjustments that can significantly alter the reported gain and the ROU asset value.

Economic deal analysis: What numbers really matter?

Accounting classification tells you how to report the deal. Economic analysis tells you whether it is actually a good deal. These are two separate exercises, and both are essential. A two-track analysis covering accounting classification alongside transaction underwriting economics, including cap rate, rent-to-value, escalation structure, re-lease risk, and capital expenditure allocation, is the professional standard for evaluating these transactions.

Cap rate and sale price

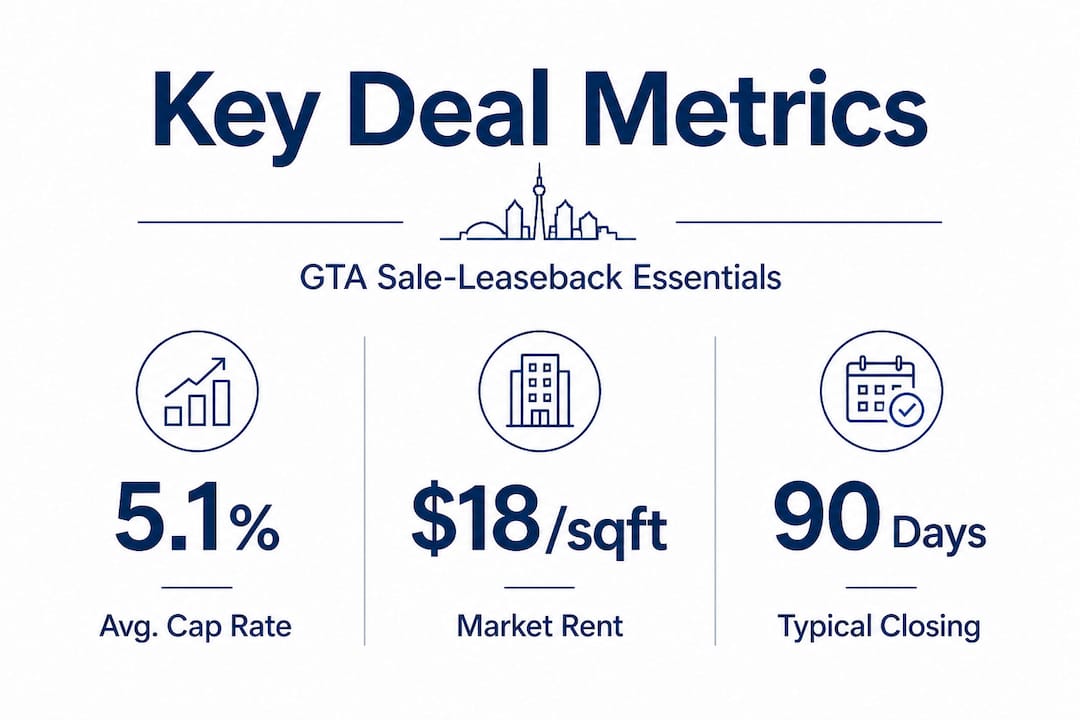

The capitalisation rate (cap rate) is the primary valuation tool for industrial investment properties. It is calculated as net operating income divided by property value. In the GTA, industrial cap rates have compressed significantly over recent years. Prime logistics assets in Mississauga and Brampton have traded in the 4.5 to 5.5 percent range, while secondary markets like Oshawa or Hamilton have seen rates in the 5.5 to 6.5 percent range. A lower cap rate means a higher sale price for the seller.

Rent benchmarks and stress-testing

| Variable | GTA prime (Mississauga/Brampton) | GTA secondary (Durham/Hamilton) |

|---|---|---|

| Typical net rent (per sq ft) | $16 to $20 | $12 to $15 |

| Annual escalation (typical) | 2 to 3% | 2 to 3% |

| Lease term (typical leaseback) | 10 to 15 years | 7 to 12 years |

| Cap rate range | 4.5 to 5.5% | 5.5 to 6.5% |

Key economic variables to stress-test:

- What happens to your occupancy cost if rent escalates at 3 percent annually for 15 years?

- Who is responsible for roof replacement, HVAC, or structural repairs?

- What is the re-lease risk if you vacate at lease expiry and the market has softened?

- Does the escalation clause include a cap, or is it uncapped CPI-linked?

- Are there renewal options, and at what rent reset mechanism?

To maximise property returns on the buyer side, investors typically seek above-market escalation and minimal landlord capital obligations. As the seller-tenant, you want the opposite. Negotiating these terms carefully is where real value is created or lost.

Consider property upgrades for value before entering a leaseback. A well-maintained asset with recent capital improvements commands a higher sale price and gives you leverage to negotiate favourable lease terms.

Due diligence and risk management essentials

Economic analysis and accounting classification are only as reliable as the underlying facts. Due diligence is where you verify those facts and identify risks that could undermine the deal's value after closing.

Edge-case due diligence for sale-leasebacks must include, at minimum: a property condition assessment, zoning and certificate of occupancy review confirming rebuild legality, title and survey review for encumbrances and encroachments, an environmental site assessment, and a clear understanding of how risks fall back to the owner if the lease ends or for strict-liability environmental items.

Critical diligence steps:

- Physical inspection. Commission a full property condition assessment. Identify deferred maintenance and confirm who is responsible for major capital items under the proposed lease.

- Zoning and permits. Confirm the property is zoned for the intended industrial use. Verify that any existing or planned improvements comply with current zoning bylaws. Non-conforming uses create significant re-tenanting risk.

- Title and survey review. Engage a real estate solicitor to review the title for encumbrances, restrictive covenants, or easements that could limit use or value.

- Environmental assessment. Obtain a Phase I ESA. If any recognised environmental conditions are identified, proceed to Phase II. Environmental liability in Ontario can be strict and can fall back to the landowner regardless of lease terms.

- Lease structure review. Confirm that the leaseback lease clearly allocates repair, maintenance, and capital expenditure obligations. Ambiguity here is expensive.

- Exit scenario modelling. Model what happens if the tenant (you) defaults, exits early, or if the property requires rezoning for a future buyer. Understanding the lease agreement basics helps clarify what protections are standard and what must be negotiated.

Expert caution: Always stress the exit and contingency risk: analyse what happens if the tenant fails, if the lease terminates early, or if redevelopment or re-tenanting requires zoning compliance or capital that the lease does not fully allocate away from the landlord. In the GTA, where redevelopment pressure is high, this scenario is more likely than many buyers anticipate.

The due diligence checklist provides a structured framework to ensure no critical item is overlooked during the verification phase.

Why economic and accounting analysis both matter more than most think

Here is what we see repeatedly in the GTA market: owners focus almost entirely on the economics. The sale price looks strong, the cap rate is favourable, and the rent seems manageable. They sign. Then, six months later, they discover that the accounting treatment of the deal created an unexpected tax consequence, or that the off-market rent they agreed to has triggered a measurement adjustment that inflates their reported lease liability.

The reverse also happens. A sophisticated operator spends weeks on accounting classification, confirms the deal qualifies as a true sale under IFRS 15, and then fails to adequately stress-test the rent escalation structure. Ten years into a 15-year lease with uncapped CPI escalation, their occupancy cost has grown 40 percent and is now materially above market. The accounting was clean. The economics were not.

The uncomfortable truth is that these two analyses are deeply interconnected. Off-market lease terms affect both the accounting measurement and the economic value of the deal. A sale price above market value is not just an accounting adjustment; it signals that the buyer is pricing in above-market rent, which means your long-term occupancy cost is embedded in the "premium" you received. That is not free money.

In the GTA, deal velocity is high. Buyers are motivated and often push for quick closings. That pressure creates shortcuts. We have seen owners skip the Phase II environmental assessment to meet a buyer's timeline, only to face remediation liability years later when the lease ended. We have seen buyers accept seller representations on zoning without independent verification, then discover the property's mezzanine office was never permitted.

The investment sales insights we have gathered from GTA transactions consistently point to one lesson: the owners who get the best outcomes model both the accounting and economic paths before entering negotiations, then get independent professional review before signing. In a market this competitive, diligence shortcuts rarely pay off.

Next steps: How expert guidance helps you win on GTA leaseback deals

Navigating a sale-leaseback transaction in the GTA requires more than a spreadsheet. The interplay between accounting standards, market economics, and physical due diligence demands specialised expertise at every stage.

At Michael Law Real Estate, we work with industrial property owners, investors, and corporate tenants across the GTA to structure, evaluate, and close leaseback transactions with confidence. Whether you are assessing your first leaseback or optimising a portfolio of industrial assets, our team delivers the market intelligence and transaction expertise you need. Explore GTA commercial listings to see current opportunities, or review active deals in Milton and Caledon where leaseback structures are increasingly common. Contact us for a personalised assessment of your property's leaseback potential.

Frequently asked questions

How do I know if my leaseback deal qualifies as a true sale under IFRS 16?

You must determine if control of the property transfers to the buyer using IFRS 15 criteria; if control does not transfer, the deal is treated as a financing arrangement with no gain recognised.

What documents do I need to analyse a leaseback deal in the GTA?

Key documents include the property title, existing lease, site surveys, zoning certificates, and an updated environmental site assessment, as core diligence items that protect both buyer and seller.

How are off-market lease terms treated in a sale-leaseback transaction?

If lease payments are above or below market, IFRS 16 requires adjustments to recognise prepaid rent or additional financing, which directly affects the reported gain and the ROU asset value.

What are the most common risks in GTA sale-leaseback deals?

Risks include tenant default, environmental liabilities, zoning or title issues, and ambiguity about capital expenditure responsibilities, all of which can fall back to the landlord if the lease ends or strict-liability items arise.