Many investors and tenants in the Greater Toronto Area industrial market face unexpected costs when they sign net leases without fully understanding expense allocations. The confusion around who pays property taxes, insurance, and maintenance often leads to budget surprises and strained landlord-tenant relationships. This guide clarifies net lease structures, explains the differences between single, double, and triple net leases, and provides actionable strategies to evaluate and negotiate these agreements effectively in GTA industrial properties.

Table of Contents

- Key takeaways

- What is a net lease and how does it work?

- Types of net leases and how they differ

- Common challenges and nuances in net lease agreements

- How to evaluate and negotiate net leases in the GTA industrial market

- Discover expert commercial real estate services in GTA

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cost shifting basics | Net leases move property taxes, insurance and maintenance costs from the landlord to the tenant, affecting the total occupancy costs. |

| Lease type differences | Single, double and triple net leases allocate expenses differently, so compare total occupancy costs rather than base rent alone. |

| CAM charges clarity | Always request a detailed three year CAM breakdown to spot spikes and negotiate exclusions. |

| Budget alignment strategies | Evaluate proposals by normalising costs to a fully serviced equivalent rate to avoid inflated expense pass through. |

What is a net lease and how does it work?

A net lease is a commercial lease where the tenant pays base rent plus some or all of property taxes, insurance, and maintenance costs. This structure shifts operating expenses from landlord to tenant, fundamentally changing the financial dynamics of the tenancy. Unlike gross leases where landlords absorb all property operating costs, net leases make tenants responsible for specific expense categories beyond their monthly rent payments.

The mechanics work through a combination of base rent and additional charges. Tenants pay a lower base rent compared to gross leases, but they also receive monthly or quarterly invoices for their share of operating expenses. These additional costs typically include property taxes, building insurance premiums, and common area maintenance charges. The allocation method depends on whether the property houses a single tenant or multiple tenants, with multi-tenant buildings using proration formulas based on each tenant's occupied square footage.

In GTA industrial properties, net leases dominate the market because they provide landlords with predictable income streams while protecting them from rising operating costs. For example, a warehouse tenant in Mississauga might pay base rent of $8 per square foot annually, plus their proportionate share of property taxes averaging $3 per square foot, insurance at $0.50 per square foot, and maintenance costs of $2 per square foot. This transparency allows tenants to budget accurately, but only if they thoroughly understand what expenses the lease includes.

The relationship between base rent and additional charges varies significantly across different net lease structures. Some landlords price base rent aggressively low to attract tenants, then recover profits through operating expense charges. Others maintain market-rate base rents with reasonable expense pass-throughs. This variation makes comparing lease proposals challenging without normalising all costs to a fully serviced equivalent rate.

Common components in net leases extend beyond the basic trio of taxes, insurance, and maintenance. Depending on the lease type, tenants may also pay for utilities, janitorial services, snow removal, landscaping, security, and building management fees. Commercial real estate expertise becomes essential when evaluating which expenses are reasonable and market-standard versus which represent landlord cost-shifting.

Pro Tip: Always request a detailed breakdown of CAM charges for the previous three years before signing a net lease. This historical data reveals expense trends and helps you identify unusual spikes or non-standard charges that warrant negotiation or exclusion from your lease agreement.

Types of net leases and how they differ

Net leases exist in three primary forms, each allocating different expense responsibilities between landlord and tenant. Understanding these distinctions helps you assess the true cost of occupancy and compare proposals accurately across industrial property listings in the GTA market.

| Lease type | Tenant pays | Landlord pays | Common in |

|---|---|---|---|

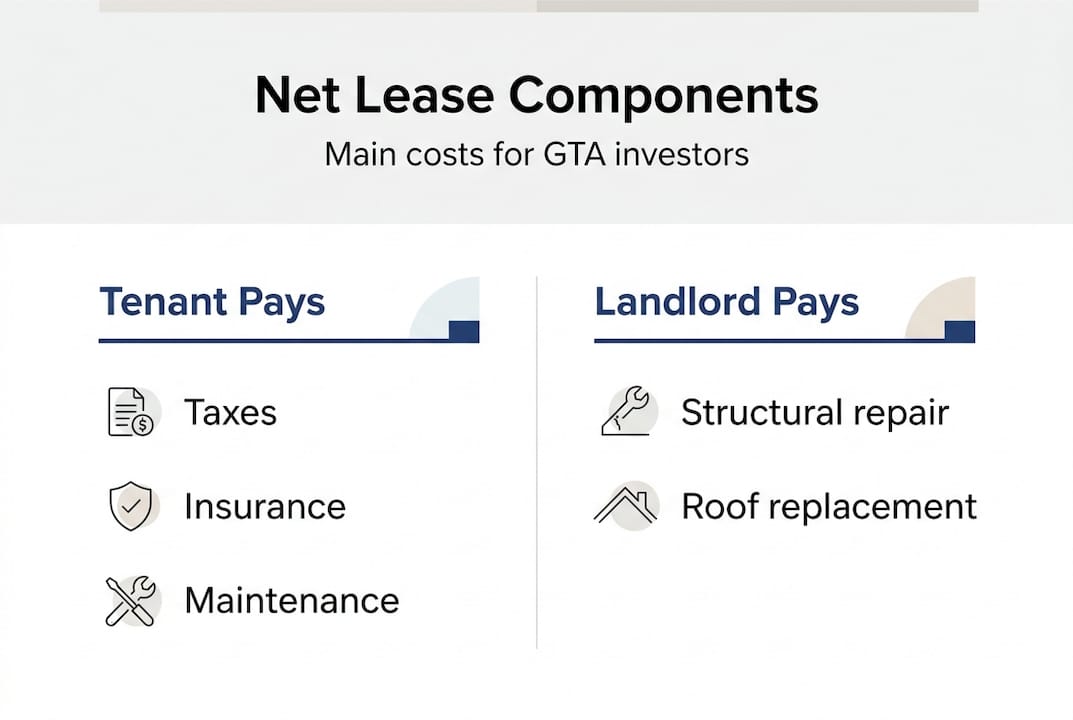

| Single net (N) | Property taxes | Insurance, maintenance, repairs | Older properties, transitional arrangements |

| Double net (NN) | Property taxes, insurance | Maintenance, structural repairs | Multi-tenant industrial buildings |

| Triple net (NNN) | Property taxes, insurance, maintenance | Structural repairs (roof, foundation) | Most GTA industrial properties |

| Absolute NNN | All expenses including structural | Nothing | Build-to-suit, sale-leaseback transactions |

Single net leases represent the most landlord-friendly structure among the three main types. Tenants pay only property taxes beyond base rent, while landlords retain responsibility for insurance premiums and all maintenance costs. This arrangement rarely appears in modern GTA industrial leases because landlords prefer greater expense protection. You might encounter single net structures in older buildings where landlords maintain tight control over property management or in short-term transitional leases.

Double net leases add insurance premiums to the tenant's expense burden. Beyond base rent and property taxes, tenants now cover the building's insurance costs while landlords handle maintenance and repairs. This structure appears more frequently in multi-tenant industrial properties where landlords want to protect against insurance rate increases but maintain control over building upkeep quality. The challenge lies in verifying that insurance premiums reflect actual coverage costs rather than inflated charges.

Triple net leases dominate the GTA industrial market, with tenants paying property taxes, insurance, and maintenance costs alongside base rent. Landlords typically retain responsibility only for major structural repairs like roof replacement or foundation work, though lease language varies significantly. Monthly estimates for these expenses create predictable cash flow, with annual true-up reconciliations adjusting for actual costs incurred. Proration by gross leasable area ensures fair allocation in multi-tenant buildings, though vacancy exclusions and gross-up provisions add complexity.

True-up reconciliations occur annually, comparing estimated payments against actual expenses. If estimates exceeded actual costs, landlords refund the difference. If actual costs surpassed estimates, tenants pay the shortfall. This process requires detailed accounting and creates opportunities for disputes if landlords include inappropriate expenses or miscalculate prorations. Escalation clauses further complicate matters by increasing base rent or expense estimates annually through fixed percentages or Consumer Price Index adjustments.

Here's how expense calculations and reconciliations typically work:

- Landlord estimates annual operating expenses and divides by 12 for monthly charges.

- Tenant pays monthly estimates alongside base rent throughout the lease year.

- Landlord compiles actual expenses at year-end and calculates each tenant's proportionate share.

- Proportionate share equals tenant's square footage divided by building's total gross leasable area.

- Landlord compares actual proportionate share to total estimates paid and invoices difference or issues refund.

- Tenant exercises audit rights if reconciliation reveals unexpected increases or questionable charges.

Gross leasable area calculations significantly impact expense allocation in multi-tenant properties. Some landlords include vacant space in the denominator, reducing each tenant's proportionate share. Others exclude vacancies, increasing occupied tenants' expense burden. This distinction can shift thousands of dollars in annual costs, making it a critical negotiation point in lease agreements.

Common challenges and nuances in net lease agreements

Absolute triple net leases push expense responsibility to its extreme, requiring tenants to pay for structural repairs including roof replacement, foundation work, and major building system overhauls. These arrangements typically appear in build-to-suit developments or sale-leaseback transactions where tenants occupy entire buildings long-term. The financial implications prove substantial, as structural repairs can cost hundreds of thousands of dollars unexpectedly. Few tenants possess the financial reserves or risk appetite for absolute triple net structures unless they receive significant base rent concessions.

CAM charge disputes represent the most common source of landlord-tenant friction in net lease arrangements. Landlords sometimes disguise capital expenditures as operating expenses, improperly charging tenants for improvements that increase property value rather than maintain existing conditions. For example, a landlord might classify a parking lot expansion as maintenance rather than capital improvement, spreading costs across all tenants despite the enhancement primarily benefiting new tenants or increasing property value. GAAP accounting standards require capital expenditures to be amortised over their useful life, not expensed immediately, but enforcement depends on lease language and tenant vigilance.

Gross-up calculation errors create another frequent problem in multi-tenant buildings with vacancy. When calculating operating expenses, landlords should exclude variable costs that decrease with vacancy, like utilities and janitorial services, from gross-up formulas. However, fixed costs like property taxes and insurance legitimately get grossed up as if the building were fully occupied, preventing occupied tenants from subsidising vacant space. Landlords sometimes incorrectly gross up variable expenses or fail to gross up fixed expenses, distorting each tenant's fair share. These errors can inflate your costs by 15-25% in buildings with significant vacancy.

Audit rights provide essential protection against CAM overcharges and calculation errors. Standard lease language allows tenants to examine landlord books and records annually, typically at tenant expense unless the audit reveals overcharges exceeding 5% of billed amounts. Without explicit audit rights in your lease, you have no legal mechanism to verify expense accuracy. Many tenants never exercise these rights due to cost concerns, but professional audit firms work on contingency, charging fees only when they recover overcharges.

Multi-tenant proration complexities extend beyond vacancy considerations. Tenants must verify that the denominator in proportionate share calculations includes only leasable space, not common areas, mechanical rooms, or other non-leasable square footage. Some landlords inflate the denominator to reduce their own proportionate share in buildings where they occupy space, effectively shifting costs to tenants. The numerator should reflect your actual leased square footage as measured by the same standard used for the denominator, whether that's BOMA, ANSI, or another measurement methodology.

Pro Tip: Negotiate a cap on annual CAM increases at 3-5% to protect against unexpected expense spikes. This provision limits your exposure while still allowing landlords to pass through reasonable cost increases, creating a balanced risk-sharing arrangement that benefits both parties.

Audit rights are essential tenant protection mechanisms that enable verification of landlord operating cost claims, prevent overcharges, and ensure compliance with lease terms and accounting standards.

How to evaluate and negotiate net leases in the GTA industrial market

Systematic evaluation prevents costly mistakes and positions you to negotiate favourable terms. Follow these steps when reviewing net lease proposals:

- Request three years of historical operating expenses to establish baseline costs and identify trends that inform your budget projections and negotiation strategy.

- Calculate total occupancy cost by adding base rent plus average annual operating expenses, then compare this figure across multiple properties to identify true value.

- Verify that the lease defines operating expenses clearly, excluding capital improvements, leasing commissions, and landlord profit margins from CAM charges.

- Confirm proration methodology excludes vacant space from variable expense calculations while appropriately grossing up fixed costs to prevent cost-shifting.

- Negotiate audit rights with provisions requiring landlord to pay audit costs if overcharges exceed 5%, creating accountability without upfront expense.

- Establish expense caps or collars limiting annual increases to protect against market volatility while maintaining landlord incentive to control costs.

Verifying CAM and operating expense estimates requires detailed analysis of landlord-provided financial statements. Compare estimated costs against market benchmarks for similar GTA industrial properties, questioning any line items that exceed typical ranges. Property taxes should align with municipal assessment values and current mill rates. Insurance premiums should reflect actual coverage costs, not inflated amounts that generate landlord profit. Maintenance costs vary by building age and condition, but you can establish reasonable ranges through industrial property management services familiar with local market standards.

Expense proration verification ensures you pay only your fair share in multi-tenant buildings. Request a rent roll showing all tenants, their square footage, and lease terms to calculate the building's total gross leasable area. Confirm this figure matches the denominator in your proportionate share calculation. Examine how the landlord treats vacant space, amenity areas, and common facilities. Some landlords include fitness centres or cafeterias in gross leasable area despite these spaces generating no rental income, artificially reducing all tenants' proportionate shares.

Negotiating audit rights and true-up timing protects your interests throughout the lease term. Standard language allows audits within 90-180 days after receiving annual reconciliation statements, but you should negotiate for 12-month audit windows to allow thorough review. True-up timing matters because delayed reconciliations create cash flow uncertainty. Negotiate for reconciliation statements within 90 days of year-end, with any tenant payments due 30 days after statement delivery. This timeline provides landlords adequate preparation time while preventing indefinite delays.

Key clauses requiring scrutiny include expense definitions, exclusions, caps, and dispute resolution procedures. Your lease should explicitly exclude capital expenditures, financing costs, leasing commissions, and landlord administrative overhead beyond reasonable management fees. Commercial real estate consulting expertise helps identify problematic language that shifts inappropriate costs to tenants. Dispute resolution clauses should specify mediation or arbitration procedures, avoiding costly litigation when disagreements arise.

Pro Tip: Engage a commercial real estate lawyer and accountant to review complex net lease agreements before signing. Their combined expertise identifies hidden costs, problematic clauses, and negotiation opportunities that protect your investment and prevent disputes throughout the lease term.

Escalation clauses deserve particular attention because they compound over time, significantly impacting long-term occupancy costs. Fixed percentage increases of 2-3% annually provide predictability but may exceed actual expense growth during stable economic periods. CPI-linked escalations better reflect true cost changes but introduce uncertainty during inflationary periods. Consider negotiating hybrid approaches that use CPI increases capped at maximum percentages, balancing flexibility with protection. Real estate cost optimisation strategies help you model different escalation scenarios and their financial impact over your lease term.

Understanding landlord tenant obligations in Ontario commercial leases provides additional context for negotiation. While residential tenancy laws don't apply to commercial properties, general contract principles and commercial tenancy best practices still govern lease relationships. Clear documentation of all agreed terms prevents misunderstandings and provides enforcement mechanisms if disputes arise.

Discover expert commercial real estate services in GTA

Navigating net lease complexities requires specialised knowledge of GTA industrial real estate markets, lease structures, and negotiation strategies. Michael Law commercial real estate provides expert guidance to investors and tenants seeking to optimise their industrial property transactions. With deep market intelligence and proven negotiation expertise, professional advisory services help you avoid costly mistakes and secure lease terms that protect your financial interests.

Comprehensive commercial real estate services include lease analysis, market comparisons, and negotiation support tailored to your specific requirements. Whether you're evaluating multiple properties, renegotiating existing leases, or structuring new agreements, experienced advisors ensure you understand all cost implications and contractual obligations. Explore available commercial industrial properties with transparent lease structures and favourable terms that align with your business objectives in the Greater Toronto Area market.

Frequently asked questions

What costs are typically included in a triple net lease?

Triple net leases require tenants to pay property taxes, building insurance premiums, and common area maintenance charges beyond base rent. CAM typically includes janitorial services, snow removal, landscaping, parking lot maintenance, and building management fees. Structural repairs like roof replacement usually remain landlord responsibility unless the lease specifies absolute triple net terms.

How often are true-up reconciliations done in net leases?

True-up reconciliations occur annually, comparing estimated operating expense payments against actual costs incurred during the lease year. Landlords typically provide reconciliation statements within 90-120 days after year-end, though lease terms vary. Tenants then pay any shortfall or receive refunds for overpayments within 30 days of statement delivery.

What does audit rights mean in a commercial lease?

Audit rights allow tenants to examine landlord books and records to verify operating expense accuracy and proper proration calculations. Standard provisions permit audits within 90-180 days of receiving annual reconciliation statements, typically at tenant expense unless overcharges exceed 5%. This protection mechanism prevents CAM overcharges and ensures lease compliance.

Can tenants negotiate which expenses they pay under a net lease?

Yes, tenants can negotiate expense exclusions, caps, and allocation methods during lease negotiations. Common exclusions include capital improvements, leasing commissions, and landlord administrative overhead beyond reasonable management fees. Expense caps limit annual increases to 3-5%, protecting against unexpected spikes. Negotiation success depends on market conditions, tenant leverage, and landlord flexibility.

How does vacancy affect expense prorations?

Vacancy impacts expense prorations differently for fixed versus variable costs. Fixed expenses like property taxes and insurance get grossed up as if the building were fully occupied, preventing occupied tenants from subsidising vacant space. Variable expenses like utilities and janitorial services should not be grossed up since they decrease with vacancy. Proper lease language ensures fair allocation regardless of building occupancy levels.