TL;DR:

- Most corporate tenants treat lease renewal as a routine event, missing opportunities to leverage financial negotiations.

- Proper early planning, market intelligence, and professional representation enable tenants to secure substantial cost reductions and flexible terms.

Most corporate real estate managers treat lease renewal as a calendar event rather than a negotiation. That framing is expensive. Understanding why lease renewal matters for corporations goes far beyond avoiding a holdover clause or locking in another five years at a familiar address. It means recognising a timed window where the financial terms of your entire occupancy can be reset, where you hold more leverage than at any other point in the tenancy cycle, and where preparation separates companies that reduce costs from those that simply absorb them. In the GTA industrial market especially, where vacancy remains structurally constrained and rents have climbed sharply across nodes from Brampton to Durham Region, renewal decisions carry millions of dollars in consequence.

Table of Contents

- Key takeaways

- Why lease renewal matters for corporations in the GTA industrial market

- Lease provisions every corporate tenant must review

- Pitfalls that cost corporations millions at renewal

- How to build and execute a renewal strategy that works

- IFRS 16 and the accounting dimension of renewal decisions

- My perspective on what most corporations get wrong

- Work with Mlawrealestate on your next GTA lease renewal

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Renewal is a strategic event | Treat lease renewal as a major financial negotiation, not a routine administrative task. |

| Start 18 to 36 months early | Beginning the process early preserves tenant leverage and expands your alternatives before expiry pressure builds. |

| Total cost exceeds base rent | Operating expenses, CAM charges, and escalations can add 30 to 40 per cent above base rent if left uncapped. |

| IFRS 16 has real consequences | Renewal decisions directly affect right-of-use asset accounting and lease liabilities on your financial statements. |

| Professional representation matters | A tenant rep with current GTA market intelligence materially improves negotiation outcomes across all deal components. |

Why lease renewal matters for corporations in the GTA industrial market

Lease renewal is one of the most financially significant decisions a corporation makes within its real estate portfolio. Yet most organisations walk into it with the same preparation they would bring to renewing a software subscription. That gap between the stakes and the attention paid is precisely where occupancy costs expand unnecessarily.

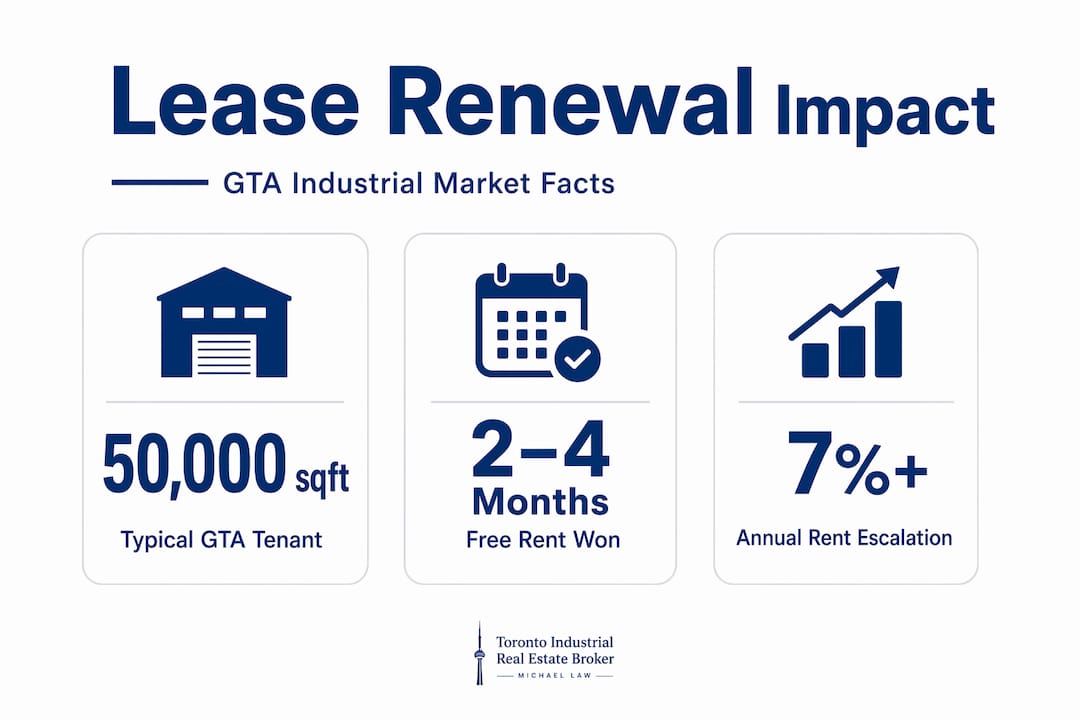

For a GTA industrial tenant occupying, say, 50,000 square feet in Mississauga or Vaughan, a renewal negotiated at even $2 per square foot below market rate translates to $100,000 per year in savings over a five-year term. That is real capital that flows back into operations, capital expenditure, or headcount. The impact of lease terms on business performance is direct, compounding, and largely invisible until someone adds it up.

The landlord's calculus is the tenant's opportunity. Replacing a creditworthy, established tenant is expensive. Replacing a single tenant for a 5,000 square foot lease can cost a landlord approximately $350,000 in combined lost rent, broker commissions, tenant improvement allowances, and free rent. For larger GTA industrial footprints, that number scales significantly. Landlords know this. Tenants who understand it negotiate from a position of genuine strength.

In the GTA specifically, several market forces shape the renewal environment:

- Constrained supply: Vacancy across major industrial corridors including Brampton, Markham, and the Airport submarket has remained historically low, limiting a tenant's ability to relocate on short notice.

- Rising replacement rents: New asking rates frequently exceed in-place rents by a meaningful margin, making renewal at the right terms preferable to relocation for both parties under the right conditions.

- Landlord sensitivity to downtime: Extended vacancy is punishing in a market where carrying costs are high and institutional landlords manage portfolio metrics closely.

- Submarket variability: Renewal dynamics in Ajax or Oshawa differ from those in Mississauga or Burlington. Hyper-local intelligence determines whether a proposed rent represents a discount or a penalty.

Corporate leasing strategies that account for these dynamics treat renewal not as a formality but as a scheduled negotiation requiring data, alternatives, and professional execution.

Lease provisions every corporate tenant must review

Walking into a renewal conversation without a thorough lease audit is one of the most common and costly errors in corporate real estate management. The existing lease defines the baseline, and the renewal negotiation is the one moment where that baseline can be substantively changed. Knowing which clauses to challenge and which concessions to request changes the financial outcome materially.

Rent adjustment and escalation mechanisms

Most industrial leases in the GTA include annual rent escalations built into the renewal term. These are often presented as fixed and non-negotiable. They are not. CAM caps negotiated at 3 to 5 per cent annually are standard in well-structured renewals. Without a cap, operating expense pass-throughs can erode the value of a seemingly attractive base rent within two years of the renewal commencement date.

Contraction and expansion rights

Hybrid and flexible operating models have changed how corporations think about footprint. Contraction rights allowing up to 20 per cent space reduction are increasingly common in renewal terms for tenants with the leverage and the data to support the request. Expansion rights matter equally for growth-oriented operators in logistics or e-commerce who anticipate throughput increases.

Tenant improvement allowances and free rent

These are the most tangible concessions available at renewal. Tenants with strong leverage commonly achieve two to four months of free rent and tenant improvement allowances ranging from $15 to $80 per square foot. The range is wide because it depends on lease term length, tenant credit, and the credibility of alternatives. Practical tenant improvement examples illustrate how these allowances translate into facility upgrades that directly benefit operations.

Renewal notice deadlines

This is the clause that ends careers and costs corporations the most in avoidable losses. Courts enforce time-of-the-essence clauses strictly, often voiding renewal rights for even minimal delays. Missing a notice deadline can force a tenant into a holdover position, renegotiating from scratch without any of the leverage the renewal option would have provided.

Pro Tip: Set calendar reminders at 24 months, 18 months, 12 months, and 90 days before each renewal notice deadline. Assign accountability to a named individual, not just a department. A detailed lease abstraction process at the outset of each tenancy prevents this failure mode entirely.

Pitfalls that cost corporations millions at renewal

Understanding what to do is only half the picture. The other half is recognising the mistakes that experienced tenants still make, often because the renewal process is poorly institutionalised within the corporate real estate function.

-

Treating renewal as passive. Many corporate tenants send back the landlord's renewal proposal with minor edits and call it done. This approach hands the landlord the negotiating framework entirely. You are now reacting to their terms rather than setting the agenda.

-

Starting too late. Best practice is to begin the renewal diagnostic 18 to 36 months before lease expiry. Negotiations started within six months of expiry give landlords near-total leverage because the tenant has no credible relocation window remaining.

-

Focusing only on base rent. Total occupancy costs routinely exceed base rent by 30 to 40 per cent once operating expenses, property taxes, insurance, and management fees are added together without caps. A tenant who wins on net rent but concedes on expense structure can still overpay significantly.

-

Failing to develop credible alternatives. Leverage at renewal derives from credible alternatives, not from goodwill or tenure. A well-documented alternative property proposal changes the negotiating dynamic immediately. Without one, the landlord has no reason to move off their opening position.

-

Ignoring space utilisation data. Companies can reduce their real estate footprint by up to 30 per cent when renewal negotiations are informed by actual occupancy and throughput data. Renewing based on historical footprint rather than current need locks in years of overpayment.

-

Missing legal deadlines. As noted above, this is the single most irreversible mistake available in the renewal process. Once a notice window closes, the legal position changes fundamentally.

Pro Tip: Before entering any renewal negotiation, prepare a two-page summary of your current lease economics, market alternatives within your operational radius, and the key terms you intend to renegotiate. This document disciplines your team's thinking and signals preparation to the landlord.

How to build and execute a renewal strategy that works

Effective lease management for companies that operate significant industrial footprints requires a structured process, not an ad hoc response to a landlord's renewal notice. The following framework reflects what high-performing corporate real estate functions actually do.

Timeline and preparation

| Phase | Timeframe before expiry | Key activities |

|---|---|---|

| Strategic review | 36 to 30 months | Audit lease economics, assess space utilisation, identify operational requirements for next term |

| Market intelligence | 30 to 24 months | Survey comparable properties, engage tenant representation, document credible alternatives |

| Negotiation | 24 to 12 months | Issue renewal proposal, negotiate rent, TI, free rent, escalation, and flexibility provisions |

| Legal review | 12 to 6 months | Engage legal counsel to review final terms, confirm notice obligations, execute renewal |

| Documentation | 6 months to closing | Complete lease abstraction, set deadline tracking systems for the new term |

This timeline gives you the negotiating room to walk away if the landlord's position is unreasonable. That walk-away credibility is precisely what drives concessions.

What to negotiate beyond rent

Experienced GTA industrial tenant representatives negotiate the full economic package, not just the headline rate. The list of items in play at renewal includes:

- Base rent and annual escalation rate or mechanism

- Gross-up provisions and operating expense caps

- Tenant improvement allowances tied to specific facility upgrades

- Free rent periods at renewal commencement

- Contraction or expansion options and their trigger conditions

- Renewal option terms for the subsequent period

- Assignment and subletting rights

Engaging a tenant rep early in this process brings market comps, landlord intelligence, and negotiation experience that internal teams rarely carry. The value of broker expertise in leasing is not limited to finding space. It is most valuable when it prevents a corporation from leaving concessions on the table at renewal. For GTA industrial tenants specifically, understanding rent escalation strategies before entering the renewal room is a material advantage.

IFRS 16 and the accounting dimension of renewal decisions

For publicly reporting corporations and many private companies, lease renewal decisions are not just occupancy decisions. They are accounting decisions with immediate consequences on the balance sheet and income statement.

Under IFRS 16, a lessee must assess whether exercising a renewal option is reasonably certain at the commencement of the lease. This assessment determines the lease term used to calculate the right-of-use asset and the corresponding lease liability. When renewal assumptions change, whether a previously excluded option becomes reasonably certain or vice versa, the standard requires reassessment and remeasurement.

The practical implications for corporate real estate managers include:

- Changes to renewal assumptions trigger remeasurement. When you decide to exercise or waive an option that was previously excluded from the lease liability calculation, the liability is recalculated using a revised discount rate. This affects both assets and liabilities on the balance sheet immediately.

- Depreciation and interest expense shift. A longer recognised lease term increases depreciation on the right-of-use asset and reconfigures the interest expense profile over the remaining term.

- Finance teams must be in the room. Strategic renewal decisions have direct financial statement implications. Corporate real estate managers who make renewal choices without coordinating with their finance and accounting counterparts create reporting surprises that auditors and boards dislike.

- Renewal length choices are capital structure decisions. A 10-year renewal with high certainty of exercise creates a materially larger balance sheet footprint than a 5-year term with options. That distinction matters for leverage ratios, covenant compliance, and investor communications.

The importance of lease renewal extends well beyond the occupancy function. It sits at the intersection of operations, finance, and corporate strategy.

My perspective on what most corporations get wrong

Over years of advising GTA industrial tenants across Mississauga, Brampton, Vaughan, and the Durham Region corridor, I have watched the same pattern repeat. A corporation with a significant industrial lease approaches expiry with 10 or 11 months to go. They have not surveyed the market. They have no credible alternatives on paper. The landlord knows this. The result is a renewal that reflects the landlord's preferences, not the tenant's leverage.

The uncomfortable truth is that renewal leverage has almost nothing to do with how long you have been a tenant or how well you have paid your rent. It has everything to do with whether the landlord believes you could realistically leave. Absent that belief, they have no financial incentive to move. Creating that belief requires documented alternatives, a credible timeline, and representation that signals you are prepared to act.

I have also seen the accounting dimension catch corporate real estate teams by surprise. A renewal decision made by the real estate group without looping in the CFO's team can create an IFRS 16 remeasurement event that appears in the quarterly results. That conversation is far easier to have before signing than after.

My advice: embed renewal planning into the corporate calendar at 36 months out. Assign cross-functional accountability that includes finance, operations, and real estate. And work with a representative who knows not just the lease terms but the specific landlord's vacancy exposure, debt position, and leasing activity in that submarket. That local knowledge is what turns a passive renewal into a genuinely strategic outcome for your organisation.

— Michael

Work with Mlawrealestate on your next GTA lease renewal

Mlawrealestate advises GTA industrial tenants on lease renewals, renegotiations, and occupancy cost reduction across all major industrial nodes from Toronto and Mississauga to Hamilton, Oshawa, and the Airport Corridor. Michael Law brings institutional-grade market intelligence, a deep transaction track record, and direct affiliation with Lennard Commercial Realty to every renewal assignment.

Whether your lease expires in 18 months or three years, the time to begin is now. Early engagement is what separates corporations that shape their renewal terms from those that simply accept them. Mlawrealestate's data-backed approach covers the full negotiation package: base rent, TI allowances, operating expense caps, free rent, and flexibility provisions that align with your operational and financial objectives.

Explore current GTA industrial properties and renewal advisory services at Mlawrealestate, and connect directly with Michael Law to discuss your portfolio's specific renewal timeline and strategy. The leverage you hold today diminishes with every month you wait.

FAQ

Why does lease renewal matter so much for corporations?

Lease renewal is the single most leveraged negotiation moment in a corporate occupancy cycle. It is the only time all major financial terms, including rent, expenses, allowances, and flexibility provisions, can be reset simultaneously. Missing or mismanaging it locks in avoidable costs for the full term ahead.

How early should a corporation start the lease renewal process?

Best practice is to begin the renewal process 18 to 36 months before lease expiry. Starting earlier preserves the tenant's ability to evaluate alternative properties and walk away, which is the foundation of negotiating leverage.

What happens if a corporation misses the renewal notice deadline?

Courts routinely enforce time-of-the-essence clauses strictly, meaning even a minor delay can void the tenant's renewal rights entirely. This forces the tenant to negotiate from scratch, often at significantly worse terms or under relocation pressure.

How do lease renewal decisions affect IFRS 16 reporting?

Under IFRS 16, a change in renewal assumptions, such as deciding to exercise an option previously excluded from the lease term, requires reassessment and remeasurement of the right-of-use asset and lease liability. This creates immediate changes to balance sheet values, depreciation, and interest expense.

What concessions can a well-prepared corporate tenant realistically achieve at renewal?

With credible alternatives and proper preparation, tenants commonly secure two to four months of free rent, tenant improvement allowances between $15 and $80 per square foot, annual expense caps of 3 to 5 per cent, and flexibility provisions such as contraction or expansion rights.