TL;DR:

- Well-structured joint ventures are essential in GTA industrial real estate due to high capital requirements and deep risks. Proper planning, clear governance, and selecting partners with complementary strengths prevent costly disputes and maximize investment success. Engaging specialized advisors and thoroughly defining deal terms early enhances opportunity realization and mitigates common pitfalls.

When capital requirements are high and risk runs deep, few strategies match the power of a well-structured joint venture. Learning how to structure joint ventures in industrial real estate is no longer optional for serious GTA investors. Warehouses in Brampton and Mississauga regularly trade above $20 million, and distribution centres in Vaughan and Ajax demand development budgets that strain even well-capitalised investors. A poorly drafted agreement, a vague governance clause, or misaligned partners can unravel a deal worth years of patient positioning. This guide walks you through every stage, from initial preparation to exit, with 2026 legal and market context built in.

Table of Contents

- Key takeaways

- Prerequisites before forming an industrial JV

- Choosing the right legal structure

- Step-by-step process to execute a JV deal

- Common pitfalls and risk management

- Governance, monitoring, and exit strategies

- My perspective on GTA industrial JV structuring

- Work with Mlawrealestate on your next industrial JV

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start with strategy, not structure | Define the project scope and business purpose before selecting a legal entity or drafting any agreement. |

| LLCs dominate GTA industrial JVs | Limited liability companies offer liability protection and tax flow-through that suits most industrial partnership arrangements. |

| Waterfall terms drive real returns | Specify preferred returns, catch-up provisions, and profit-split ratios in detail before any capital is deployed. |

| Exit clauses prevent costly disputes | Buy-sell clauses and rights of first refusal with defined timelines protect both partners when the relationship ends. |

| Governance gaps cause most failures | Decision-making thresholds and escalation procedures must be written explicitly to prevent deadlocks and litigation. |

Prerequisites before forming an industrial JV

Getting the foundations right before you sign anything is the most overlooked step in structuring real estate deals. Many investors jump to the term sheet before they have agreed on what the venture is actually trying to accomplish. As research from Bradley Law confirms, vague goals are the primary cause of JV failure, and this is especially true in the industrial sector where asset lifecycles, zoning considerations, and tenant demand vary considerably across the GTA.

Define the project scope with precision. Are you acquiring an existing logistics facility in Mississauga, developing a speculative warehouse in Brampton, or repositioning an older manufacturing building in Hamilton? Each scenario carries different timelines, capital requirements, and risk profiles. A development project in Pickering is not the same investment as buying a leased facility in Oakville, even if both involve industrial assets.

Before approaching any partner, establish the following:

- The target asset class (logistics, light manufacturing, cold storage, flex industrial)

- The geographic submarket and why it fits your investment thesis

- The projected hold period and target return on investment

- The required equity and debt capital, and who brings what

- The roles each partner will play (capital, expertise, local relationships, land)

Selecting the right partner is as consequential as finding the right property. Complementary skill sets matter far more than similar backgrounds. A developer who brings land and entitlement expertise pairs better with a capital partner who has institutional financing relationships than with another developer who owns more land. Look for partners whose strengths align with your gaps.

Non-cash contributions require particular attention. When a partner contributes land or an existing building rather than cash, the valuation methodology must be agreed upon before the partnership is formed. Non-cash contributions require certified appraisals to prevent valuation disputes later. Relying on informal estimates or historical purchase prices is a reliable path to conflict.

Tax and liability considerations should be reviewed with a qualified Canadian tax advisor before any documents are drafted. The structure you choose will affect HST treatment, capital gains obligations, and each partner's personal exposure. Do not skip this step.

Pro Tip: Prepare a one-page investment summary outlining scope, capital requirements, and partner roles before your first meeting. Partners who cannot align on this document will rarely align on the full agreement.

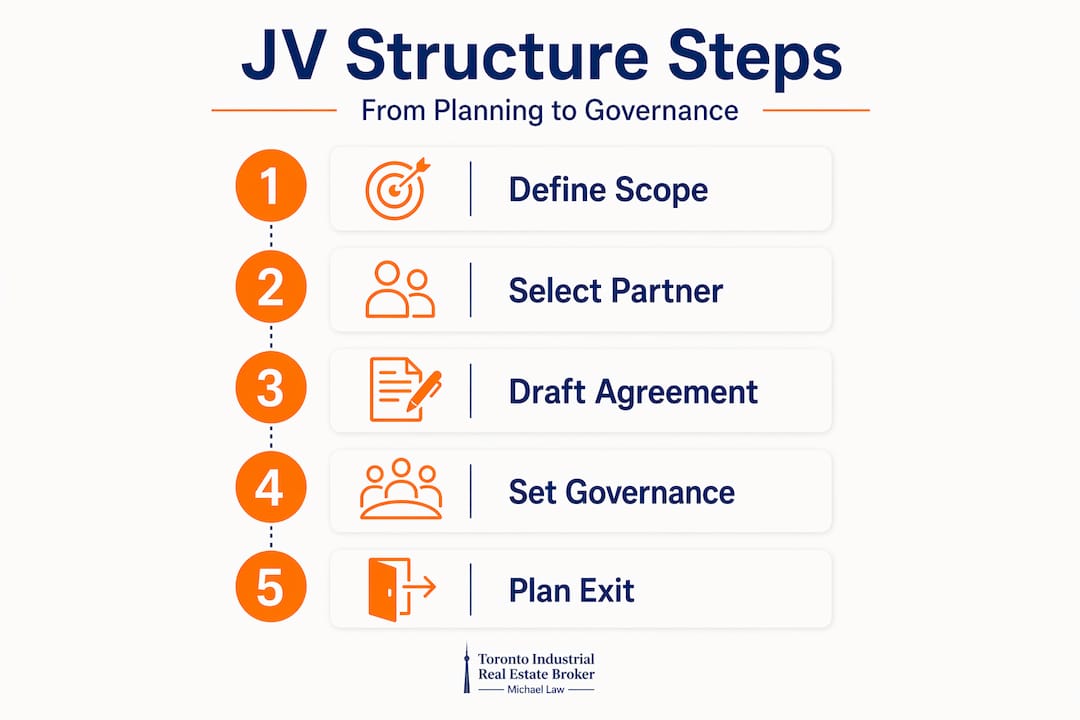

Choosing the right legal structure

The legal structure of your joint venture determines liability exposure, tax treatment, and how decisions get made day to day. Two broad categories apply to industrial real estate partnerships: equity joint ventures and contractual joint ventures.

| Structure | Key characteristics | Best suited for |

|---|---|---|

| Equity JV (LLC or LP) | Separate legal entity, shared ownership, liability protection | Development projects, multi-asset portfolios |

| Contractual JV | No new entity, parties share revenues by agreement | Single transactions, short-term collaborations |

| Limited Partnership | General partner manages, limited partners are passive | Institutional capital with passive investors |

| Co-ownership | Direct co-ownership of asset, simpler governance | Two-party acquisitions with aligned management |

LLCs are the standard choice for industrial real estate joint ventures in 2026. They offer liability protection at the entity level while allowing profits and losses to flow through to individual partners without corporate-level taxation. In the GTA context, this structure also provides flexibility to accommodate different classes of membership interest, which becomes important when structuring preferred returns for capital partners.

Once the entity type is selected, the joint venture agreement becomes the governing document for everything that follows. Think of it as a partnership constitution. The key components every industrial JV agreement must include are:

- Governance and management authority. Who controls day-to-day decisions, and which decisions require unanimous or supermajority consent? Typical reserved matters include major financing, asset sales, and material lease approvals.

- Capital contributions and capital calls. Define each partner's initial contribution, the mechanism for calling additional capital, and the consequences of failing to meet a call. Dilution clauses are common but must be carefully worded.

- Profit distribution waterfall. Specify the sequence in which cash flows are distributed, including return of capital, preferred returns, sponsor catch-up, and final profit split.

- Roles and fiduciary duties. Clarify who manages the asset, who engages third-party advisors, and what standard of care applies.

- Transfer restrictions. Define conditions under which a partner may transfer their interest and whether remaining partners hold a right of first refusal.

Operating agreements function as governance frameworks well beyond the initial financial arrangement. They govern how the partnership responds to unexpected events: a partner facing insolvency, a market downturn requiring capital injection, or a disagreement over leasing strategy.

Pro Tip: Include a tiered dispute resolution clause that escalates from direct negotiation between principals, to formal mediation, before allowing litigation. This single provision can save a partnership worth millions from unravelling over a disagreement that two calm conversations could resolve.

Step-by-step process to execute a JV deal

Knowing the components is one thing. Executing the deal is another. Here is how to move from initial alignment to a closed, structured partnership in the GTA industrial market.

- Agree on commercial terms first. Before lawyers are engaged, partners should reach written agreement on ownership percentages, contribution amounts, governance structure, and target returns. A signed term sheet or letter of intent makes the legal drafting process significantly faster and cheaper.

- Commission an independent appraisal. For any asset being contributed or acquired, obtain a current appraisal from a qualified appraiser familiar with the GTA industrial market. This applies to land contributions, existing buildings, and acquisition targets equally.

- Conduct full due diligence. Due diligence in industrial transactions covers environmental assessments, title searches, zoning and official plan compliance, lease abstracts, and structural reviews. In the GTA, confirm municipal servicing capacity and truck access compliance, as these are common deal-breakers in suburban nodes like Caledon or Oshawa.

- Negotiate the waterfall distribution structure. The waterfall sequence typically runs as follows: return of contributed capital, preferred return of 6 to 10 percent annually, a general partner catch-up provision, and then a profit split such as 80/20 or 70/30 between capital partner and sponsor. Sponsors commonly receive a carried interest or "promote" once preferred returns between 6 and 8 percent are satisfied.

- Arrange financing and understand lender requirements. Industrial acquisition and development financing in Canada typically requires 30 to 40 percent equity. Lenders frequently require joint and several liability and personal guarantees from all principals, which affects each partner's borrowing capacity on other projects. Negotiate compensation for partners who carry greater credit exposure.

- Draft and execute the JV agreement. Use counsel specialising in commercial real estate. The agreement must bind successors and assigns, and lender obligations and transfer restrictions must carry over to any party that acquires a partner's interest.

- Close the transaction and activate governance. Once title transfers or the development agreement is executed, the management structure becomes operational. Conduct an initial meeting of the management board to approve operating budgets, leasing mandates, and reporting schedules.

Key exit provisions to build in from the start:

- Buy-sell clause (shotgun provision). Either party can trigger a forced sale at a stated price, with the other party electing to buy or sell at that price. This breaks deadlocks efficiently.

- Right of First Refusal (ROFR). ROFR provisions with 30 to 60-day windows give the remaining partner adequate time to arrange financing for a buyout without creating indefinite uncertainty.

- Tag-along and drag-along rights. Tag-along rights protect minority partners when a majority partner sells. Drag-along rights allow a majority partner to compel the minority to sell on the same terms, facilitating clean exits to third parties.

- Defined valuation methodology. Agree upfront on whether exit pricing will be based on appraised value, capitalisation rate applied to net operating income, or a broker's opinion of value.

Pro Tip: Time your entry with GTA market intelligence. Submarkets like Milton and Burlington are experiencing active demand from logistics users, while some inner-Toronto nodes face redevelopment pressure. Buying into a JV at the right moment in a submarket cycle materially affects your returns. Review current GTA industrial trends before committing capital.

Common pitfalls and risk management

Most industrial real estate JVs do not fail because the asset underperforms. They fail because the partners did not anticipate specific operational or relational risks, and the agreement gave them no tools to resolve them.

The most common problems experienced advisors encounter include:

- Misaligned expectations on hold period. One partner wants to sell after three years; the other wants a ten-year hold. If the agreement does not specify a forced sale trigger or a mechanism for resolving this disagreement, the partnership becomes adversarial.

- Funding shortfalls and capital call defaults. When a partner cannot meet a capital call, the agreement must define exactly what happens. Dilution formulas should be proportional and documented. Courts in Canada have rejected punitive dilution clauses where a partner contributed significant non-cash assets and faced near-total forfeiture.

- Personal guarantee exposure. Understanding personal financial risk in JV financing is critical. A partner providing a guarantee on a $15 million industrial development loan is taking on real personal liability. Compensation for this exposure, whether through a fee, increased promote, or preferred return adjustment, should be negotiated explicitly, not assumed.

- Valuation disputes on non-cash contributions. A partner contributing land in Brampton worth an estimated $4 million who later discovers the other party believes it was worth $2.8 million creates immediate conflict. Independent, certified appraisals at contribution date eliminate this risk.

- Governance deadlocks. When two equal partners cannot agree on a material decision and the agreement provides no resolution path, the partnership can be paralysed for months.

Clear dispute resolution processes are not a sign of distrust. They are the professional standard that separates well-structured industrial real estate partnerships from expensive legal disputes.

Structured escalation from management to mediation resolves most deadlocks before they reach litigation. The sequence should be: informal discussion between principals, formal written notice, escalation to a senior management committee, then independent mediation, and finally binding arbitration or the shotgun clause if all else fails.

Pro Tip: Require quarterly financial reporting and an annual independent audit from the outset, regardless of partnership size. Partners who receive clear financial information consistently are far less likely to dispute management decisions.

Governance, monitoring, and exit strategies

Once the JV is operational, the quality of your governance framework determines whether the partnership creates or destroys value. Many investors put enormous energy into structuring the deal and very little into managing it.

Effective ongoing governance in industrial real estate partnerships includes:

- Regular management board meetings. Schedule quarterly meetings with a fixed agenda covering financial performance, leasing activity, capital expenditure approvals, and market conditions. Record decisions formally.

- Decision-making thresholds. Categorise decisions by size and consequence. Routine property management decisions may be made by the managing partner alone. Lease renewals above a set dollar threshold, capital expenditures exceeding budget, and financing decisions require full partner approval. This prevents both micromanagement and overreach.

- Performance benchmarks. Establish measurable benchmarks at the outset: target occupancy rate, net operating income, and return on equity. Review these quarterly against actuals. When the asset underperforms, partners who share a common scorecard can have productive conversations. Those who do not end up in disputes about whose fault it is.

- Financial reporting standards. Use accrual-basis accounting and produce monthly management accounts. Annual audited statements should be required by the JV agreement for any partnership managing assets above $5 million.

Exit planning should begin well before you intend to exit. In the GTA industrial market, the timing of an asset sale relative to vacancy cycles, interest rate conditions, and submarket demand significantly affects sale price. Agree on exit triggers in advance: a specific hold period, a cap rate threshold, an NOI target, or a market event.

Dissolution procedures should also be addressed in the agreement. Wind-up of a JV that has completed its purpose requires a formal resolution, distribution of remaining assets in accordance with the waterfall, and discharge of all obligations including leases, financing, and contractor commitments. Partners remain bound by confidentiality and non-compete provisions that survive dissolution, and these should be drafted with specific timelines.

When one partner exits through a buyout rather than a full asset sale, confirm that lenders approve the transfer of interest and that any guarantee arrangements are formally reassigned or released. Leaving guarantee obligations attached to a departing partner's name without formal discharge is a surprisingly common oversight with serious legal consequences.

My perspective on GTA industrial JV structuring

I have worked through enough GTA industrial deals to know that the problems investors face when structuring joint ventures are almost never about the property itself. The asset is usually sound. The issues are almost always found in the agreement, or more precisely, in what the agreement failed to address.

The most recurring mistake I see is treating the JV agreement as a formality rather than the operating manual for the partnership. Partners rush to get the deal signed, leave governance vague, and discover eighteen months later that they have fundamentally different views on leasing strategy, capital reinvestment, or when to sell. By that point, fixing the agreement costs far more than getting it right in the first place.

My honest take is that 80 percent of JV disputes are predictable and preventable. Deadlock provisions, capital call consequences, valuation methodology, and exit timelines are not difficult to draft. They just require the partners to have uncomfortable conversations before they are under pressure to have them. The investors who do that work upfront spend their time managing assets. The ones who skip it spend their time managing lawyers.

I also believe that specialized advisors are worth every dollar in complex industrial JV arrangements. A commercial real estate advisor who understands the GTA industrial market brings more than deal access. They bring knowledge of comparable transactions, lender expectations, and submarket dynamics that protect you from making structural decisions based on incomplete information. The value of a real estate advisor in this context is not about the commission. It is about avoiding a $500,000 mistake on a $10 million deal because you did not know what you did not know.

Partner selection is the single most consequential decision in a JV. Choose partners whose strengths genuinely complement yours, whose financial capacity matches their commitments, and whose values align with how you want to operate. A good deal with the wrong partner is always worse than a slightly less exciting deal with the right one.

— Michael

Work with Mlawrealestate on your next industrial JV

Structuring an industrial real estate joint venture in the GTA requires more than legal documents and a willing partner. It requires current market intelligence, transaction experience, and an advisor who understands how the pieces fit together in a market as competitive and nuanced as Toronto, Mississauga, Brampton, and the surrounding industrial corridors.

Mlawrealestate, operating through Lennard Commercial Realty, delivers precisely that. Whether you are acquiring a logistics facility, partnering on a development site in Vaughan, or repositioning an industrial asset in Hamilton, the advisory expertise at Mlawrealestate properties covers every stage of the transaction. For a direct conversation about your JV objectives and how to structure them for success, connect with Michael through his Lennard profile.

FAQ

What legal structure works best for industrial JVs in Canada?

Limited liability companies are the preferred structure for industrial real estate joint ventures in 2026 because they provide liability protection and tax flow-through without corporate-level taxation. Limited partnerships are also used when capital partners need to be passive investors.

What is a waterfall distribution in a real estate JV?

A waterfall distribution is the sequence in which cash flows are allocated among partners. It typically runs: return of capital, preferred return of 6 to 10 percent, a general partner catch-up, and then a final profit split such as 80/20 or 70/30 between capital partner and sponsor.

How do partners exit an industrial real estate joint venture?

Partners exit through a buy-sell clause, a right of first refusal, a full asset sale, or a buyout. Rights of first refusal should provide 30 to 60 days for the remaining partner to arrange financing. All exit mechanisms should be defined in the original JV agreement with clear valuation methodology.

What are the most common reasons GTA industrial JVs fail?

Most joint ventures fail due to vague governance provisions, misaligned expectations on hold period or capital contributions, and inadequate dispute resolution mechanisms. Non-cash valuation disputes and personal guarantee conflicts are also frequent sources of partnership breakdown.

Do lenders require personal guarantees in industrial JV financing?

Yes. Canadian lenders frequently require joint and several liability and personal guarantees from all principals in an industrial JV. Partners should negotiate compensation for carrying greater credit exposure, and the JV agreement should clearly address guarantee obligations and the conditions for their release.