TL;DR:

- Property valuation in the GTA considers multiple approaches, including sales, income, and cost methods, tailored to asset type and market conditions. Accurate valuation reflects physical features, tenant quality, lease terms, and location nuances, influencing leasing and investment decisions. Using comprehensive, locally informed analysis helps avoid common pitfalls and ensures more reliable market assessments.

Property valuation is frequently misunderstood as a simple exercise in pulling recent sales prices from a database. For industrial real estate investors and corporate tenants in the Greater Toronto Area, that misconception can be expensive. Property valuation estimates fair market value using evidence about the property and market conditions at a specific point in time, not a permanent figure etched in stone. A warehouse in Mississauga valued today at one number could look entirely different six months from now if a major tenant vacates or cap rates shift. Understanding what is property valuation, and how it actually works for industrial assets, is the foundation for every leasing negotiation, acquisition offer, and portfolio decision you make in the GTA.

Table of Contents

- Understanding the three main approaches to property valuation

- Applying the income approach and cap rates in the GTA industrial market

- Navigating the nuances of commercial valuation reports

- Why industrial property valuation in the GTA is more than just location and size

- How to use property valuation insights for smarter GTA industrial leasing and investment decisions

- Why many industrial property valuations miss the mark and how to avoid common pitfalls

- Michael Law commercial real estate: your partner in Toronto industrial property valuation and investment

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Valuation methods | Three main approaches—sales, income, and cost—work together to estimate industrial property value in the GTA. |

| Income approach importance | Net operating income and capitalization rates are key drivers of value for leased industrial properties. |

| Complex property factors | Utility, building features, and location nuances significantly influence valuation beyond simple metrics. |

| Valuation reports role | Comprehensive reports integrate income and lease details for informed investment and leasing decisions. |

| Expertise matters | Local market knowledge and detailed analysis prevent common valuation pitfalls for GTA industrial real estate owners. |

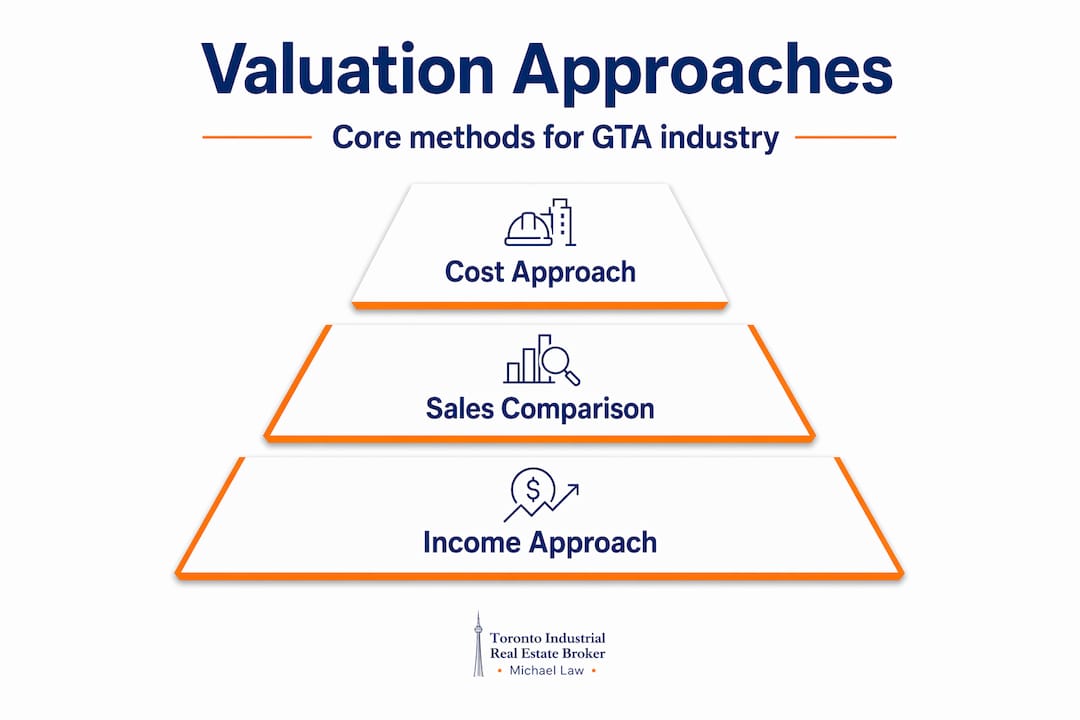

Understanding the three main approaches to property valuation

Industrial properties are not residential bungalows. They generate income, serve specialised operational needs, and vary wildly in utility depending on ceiling height, power capacity, and dock configuration. A single comparable sale rarely tells the full story. That is precisely why MPAC's valuation work incorporates three distinct approaches: sales-based evidence, income-based evidence, and cost/replacement-based evidence. Each serves a different purpose, and skilled appraisers blend them based on what the data supports.

The three core real estate valuation methods are:

- Sales comparison approach: Analyses recent transactions involving similar industrial properties to establish a market benchmark. Works best when there is an active, liquid market with enough comparable sales to draw meaningful conclusions.

- Income approach: Values the property based on its ability to generate net operating income (NOI), then applies a capitalisation rate to translate that income stream into a capital value. Dominant for leased industrial assets in the GTA.

- Cost approach: Estimates what it would cost to replace the building at today's construction prices, then subtracts depreciation. Most useful for newer specialised buildings or properties with limited comparable sales and income history.

Understanding how these approaches apply to industrial assets is where the real insight begins. A standard big-box distribution facility near the 400 corridor might have abundant sales comparables. A custom cold-storage facility with ammonia refrigeration in Etobicoke almost certainly does not. In that case, the cost approach and income approach carry far more weight.

| Approach | Best suited for | Key inputs | Limitation in GTA industrial |

|---|---|---|---|

| Sales comparison | Well-traded asset classes | Recent sale prices, size, location | Thin data for specialised buildings |

| Income approach | Leased or leasable properties | NOI, cap rates, vacancy | Requires reliable income assumptions |

| Cost approach | New or unique buildings | Replacement cost, depreciation | Can overstate value in weak markets |

Location is not just about postal code. GTA location factors such as proximity to Highway 401 ramps, distance to intermodal terminals, and labour catchment all influence which comparable sales are truly relevant and how income assumptions should be calibrated. Ignoring these nuances is one of the most common valuation errors in the market.

Applying the income approach and cap rates in the GTA industrial market

The income approach is the engine driving most GTA industrial property valuations. It answers the question every investor is actually asking: given the income this building produces, what is it worth relative to alternative investments? The mathematics are straightforward. Net operating income is calculated by taking gross rental income and subtracting operating expenses like property taxes, insurance, maintenance, and management fees. That NOI figure is then divided by the capitalisation rate to produce an indicated value.

Here is a concrete illustration. A 50,000 square foot industrial building in Brampton leased at $14 per square foot net generates $700,000 in gross rent. After $120,000 in operating expenses, NOI is $580,000. Apply a 5% cap rate and the indicated value is $11.6 million. Compress that cap rate to 4.5% because the tenant has a seven-year remaining term with strong credit and a 4.5% cap rate means paying roughly 22x annual NOI. The same income stream now indicates a value of approximately $12.9 million. That single assumption change moves the needle by $1.3 million.

Key income approach variables for GTA industrial assets:

- Contract rent vs. market rent: If the in-place rent is below market, the property may have upside value on renewal, which some buyers will pay for and others will discount due to the rollover risk.

- Lease term remaining: Longer leases with creditworthy tenants compress cap rates. Short-term leases with unknown renewal prospects push them out.

- Tenant credit quality: A publicly traded logistics company as tenant carries less income risk than a private operator with two years of operating history.

- Vacancy and absorption assumptions: The Mississauga industrial market operates differently from Etobicoke's tighter infill nodes. Vacancy assumptions must reflect the specific submarket, not GTA-wide averages.

Pro Tip: When reviewing a valuation based on the income approach, always ask what the appraiser assumed for market rent on renewal. If they used an above-market rent to sustain the value, the analysis is fragile. Realistic stabilised income assumptions are what separates a defensible valuation from an optimistic one.

Navigating the nuances of commercial valuation reports

A commercial property valuation report is not a one-page summary. For industrial assets in the GTA, a well-prepared report is a detailed analytical document that incorporates income analysis, rent schedules, operating expenses, cap rates, and lease terms to reach a defensible value conclusion. Understanding what is inside these reports, and why each element matters, makes you a far more informed buyer, seller, or tenant.

Key components of a GTA industrial valuation report:

- Property description and inspection findings: Documents physical attributes including clear height, column spacing, number of truck-level and drive-in doors, office percentage, and yard depth. These details directly affect income potential and comparable selection.

- Market overview and submarket analysis: Contextualises the subject property within current vacancy rates, absorption trends, and rental rate movements for the specific industrial node.

- Comparable sales analysis: Presents recent transactions for similar properties, with adjustments made for differences in size, location, building age, and functional utility.

- Income and expense analysis: Lays out the rent roll, operating cost breakdown, and vacancy assumptions used to derive stabilised NOI.

- Capitalisation rate selection: Explains the rationale for the chosen cap rate based on investor survey data, comparable transactions, and risk factors specific to the asset.

- Value reconciliation: Weighs the results from multiple approaches and explains which approach received the most emphasis and why.

The depth required for industrial reports far exceeds what residential appraisals demand. Understanding how investment sales work in the GTA context helps clarify why lenders, institutional buyers, and insurers all rely on these reports rather than broker opinions of value alone.

Pro Tip: Always check the effective date on a valuation report before relying on it for a transaction decision. GTA industrial market conditions can shift materially in 90 days. A report dated before a significant cap rate movement or rental rate correction may substantially misrepresent current market value.

Why industrial property valuation in the GTA is more than just location and size

Ask most people what affects property value and you get two answers: location and size. For industrial real estate in the GTA, that framing misses most of what actually drives pricing. Industrial valuation in the GTA reflects nuanced factors including ceiling height, loading dock count, column spacing, power capacity, and site circulation. A 40,000 square foot building with 28-foot clear height and eight truck-level doors commands materially different rent and cap rate treatment than an identical footprint with 20-foot clear height and two drive-in doors.

Physical and functional factors that shift industrial value in the GTA:

- Clear ceiling height: Modern logistics requirements have pushed the threshold to 28 to 36 feet for distribution users. Sub-24-foot buildings face a shrinking tenant pool and often trade at a discount.

- Loading configuration: Truck-level doors with levellers are the standard for logistics. Drive-in only configurations limit tenant options and income potential.

- Power capacity: E-commerce, cold chain, and manufacturing users increasingly require heavy power, often 2,000 to 4,000 amps at 600 volts. Buildings short on power lose entire tenant categories.

- Column spacing and bay depth: Wide-bay configurations with 50-foot-plus column spacing allow more efficient racking layouts, directly translating into higher rent tolerance from tenants.

- Site circulation and trailer parking: Last-mile and cross-dock users need room to manoeuvre 53-foot trailers. Properties without adequate yard depth or trailer storage lose competitiveness fast.

- Proximity to infrastructure: Oakville industrial properties near the QEW and 403 interchange carry a premium over otherwise similar buildings one kilometre further from the on-ramp.

| Building feature | Value impact | Tenant relevance |

|---|---|---|

| 28+ ft clear height | High positive | Distribution, e-commerce |

| Truck-level doors (multiple) | High positive | Logistics, third-party logistics |

| Heavy power (2,000+ amps) | Significant | Manufacturing, cold chain |

| Wide column spacing (50+ ft) | Moderate positive | Warehousing, racking users |

| Adequate yard/trailer parking | Moderate to high | Cross-dock, last-mile |

| Sub-20 ft clear height | Negative | Most modern users |

Understanding these factors changes how you read a property value assessment. A building that looks cheap on a per-square-foot basis may reflect genuine functional obsolescence. One that appears expensive on the same metric may be justified entirely by its physical specifications and tenant demand.

How to use property valuation insights for smarter GTA industrial leasing and investment decisions

Valuation knowledge without application is just theory. Whether you are a tenant evaluating a renewal, an investor assessing an acquisition, or an owner weighing a disposition, the goal is to translate valuation methodology into real decisions with real financial consequences.

-

Build your own stabilised income model before reviewing a listing price. Use realistic market rent for the submarket, a vacancy allowance consistent with current absorption trends, and an expense load reflective of the building's age and condition. If the asking price implies a cap rate materially below what comparable assets trade at, you need a compelling reason why, or a willingness to walk away. Small shifts in assumptions around lease terms and market rent produce meaningful changes in indicated value.

-

Map cap rates by submarket, not by GTA average. Airport corridor assets in Mississauga and Brampton historically trade at tighter cap rates than Durham Region assets. Understanding that spread tells you whether a specific asset is priced at a premium, at parity, or at a relative discount to its peers. GTA investment strategies built on submarket-level data consistently outperform decisions made on market-wide averages.

-

Separate MPAC assessed value from market value in your analysis. MPAC assessments serve a tax purpose, updated on a four-year cycle, and often diverge from current market values in fast-moving industrial submarkets. Using MPAC value as a proxy for market value in a transaction context is a fundamental error.

-

Use valuation data as a negotiating tool in lease renewals. If market rents have declined or vacancy has risen since your lease was signed, an income-approach valuation that demonstrates lower stabilised income can justify a lower renewal rate. The importance of property valuation extends well beyond acquisition. It is equally powerful as a lease negotiation instrument.

Pro Tip: When comparing a formal appraisal to a broker's opinion of value, pay attention to the income assumptions and cap rate selection, not just the headline number. Two reports can reach wildly different conclusions using the same property data simply because of different vacancy assumptions or cap rate inputs.

Why many industrial property valuations miss the mark and how to avoid common pitfalls

After working through GTA industrial transactions across the major submarkets, one pattern becomes clear: the most expensive valuation mistakes are almost never about the physical property. They are about income. Specifically, they stem from underweighting lease quality, ignoring tenant credit risk, or misapplying sales comparables from the wrong market segment.

The sales comparison approach gets misused constantly. When there are not enough truly comparable sales, appraisers sometimes reach further in time or geography to fill the grid. The result is a value conclusion anchored to transactions that reflect different market conditions, different building generations, or entirely different tenant demand profiles. A 1990s-vintage building with 22-foot clear height is not comparable to a 2015-vintage building at 32 feet, regardless of how close they are on a map.

Income analysis errors are subtler but equally damaging. A lease with two years remaining on a 25,000 square foot building tenanted by a small private company carries rollover risk that should compress value relative to a 10-year lease with an investment-grade tenant. Missing that distinction, or glossing over it in the cap rate selection, means the valuation does not reflect what an informed buyer would actually pay. As appraisers who understand GTA industrial operations recognise, the process requires translating how investors, lenders, and end users each see risk, income, and usability, and that requires genuine local market expertise.

The deeper issue is how owners and investors use valuation reports. Too often they are treated as a box-checking exercise for financing or transaction closing. The better approach is to commission valuations proactively, before going to market or renegotiating a lease, and to treat the report as a strategic planning document. What does the income profile look like if the current tenant leaves? What would this asset be worth with a 10-year lease signed at current market rent? Asking those scenario questions of a well-prepared valuation gives you a decision-making tool, not just a number on a page. The Michael Law blog regularly explores these analytical frameworks for GTA industrial investors and tenants who want to move beyond surface-level market intelligence.

Michael Law commercial real estate: your partner in Toronto industrial property valuation and investment

Understanding property valuation methodology is one thing. Applying it accurately to GTA industrial assets in motion requires current market data, transaction experience, and submarket-level relationships that take years to build.

Michael Law Real Estate provides industrial property advisory services backed by institutional-grade market analysis across every major GTA industrial corridor. From lease renewals where valuation data drives the negotiation, to investment acquisitions and dispositions where precise income modelling separates good deals from costly ones, the team brings the kind of depth this market demands. Coverage extends to submarkets including Caledon's emerging industrial nodes and well beyond the 400-series highway corridors. If you are making leasing or investment decisions in GTA industrial real estate, connect with Michael Law at Lennard Commercial Realty for advisory grounded in real transaction experience.

Frequently asked questions

What is the difference between property valuation and MPAC assessed value?

Property valuation estimates fair market value for leasing or investment decisions at a specific date, while MPAC assessed value is used for property tax purposes and updated on a four-year cycle in Ontario. The two figures often diverge significantly in fast-moving industrial submarkets.

How do capitalisation rates affect industrial property value in the GTA?

Lower cap rates produce higher valuations relative to the same NOI, and GTA industrial cap rates typically range between 4% and 5% depending on location, building quality, and lease term, meaning a 0.5% cap rate difference can shift value by millions of dollars on a mid-size asset.

Why are income and lease details critical in commercial property valuation?

Industrial buildings derive their value primarily from income generation, and lease terms, tenant credit, and vacancy risk directly determine the stability and size of that income stream, which in turn drives the capitalised value conclusion.

Can I rely solely on comparable sales to value industrial properties?

No. Industrial properties often require income and cost approach analysis because specialised assets lack sufficient comparable sales, and combining sales comparison with income analysis produces a far more defensible and accurate value conclusion for complex commercial assets.